Why You Need One Month of Testing Before Trading Live

Backtesting, forward testing, and chart exercises: the three testing types every trader needs. Spend one month proving your edge before risking real capital.

Before you risk a single dollar of real capital, spend at least one month testing your trading strategy through backtesting, forward testing, and chart exercises. These three testing types build on each other. Backtesting proves the strategy works on historical data. Forward testing proves it works in real time. Chart exercises sharpen your pattern recognition between sessions. Together, they give you something most traders never have when they go live: evidence.

The traders who skip testing are the same traders who blow accounts in their first month. Not because their strategy is bad, but because they have no data, no confidence, and no ability to distinguish between a normal losing streak and a broken system.

TL;DR

Spend at least one month testing before trading live. No exceptions.

Use three testing methods: backtesting (historical replay), forward testing (live demo), and chart exercises (static markup).

Backtesting builds your initial data set and proves the strategy has an edge.

Forward testing validates that edge under real-time conditions where emotions and execution gaps appear.

Chart exercises train your eye to spot setups faster and build confidence in your markup skills.

Only go live when your data shows positive expectancy, consistent results, and at least 80% rule adherence.

The Mistake of Skipping the Testing Phase

You find a strategy. It looks good on a YouTube video. The person teaching it is profitable. So you open a live account, deposit your savings, and start trading.

First trade: loss. Second trade: loss. Third trade: you panic, widen your stop, and lose even more. By the end of week one, you are down 8% and questioning everything.

Sound familiar? This is the most common path in trading, and it is entirely avoidable.

The problem is not the strategy. The problem is that you never tested whether you can execute it. There is a massive gap between understanding a strategy and executing it profitably in real time. Testing closes that gap.

Think about it the way you would approach any other skill. You would not enter a boxing match after watching a few fights on TV. You would not perform surgery after reading a textbook. Trading is a performance skill. It requires practice under conditions that mimic the real thing.

Walkthrough: The Cost of Skipping Testing

A trader opens a $10,000 live account with no testing. He has a supply and demand strategy that he learned from a video. He risks 2% per trade ($200) with a 1:2 reward-to-risk ratio.

Week 1: 8 trades. 3 wins ($400 each = $1,200 total), 5 losses ($200 each = $1,000 total). Net: +$200. Looks fine.

Week 2: He gets overconfident. Takes 14 trades (double the volume). 4 wins ($400 each = $1,600), 10 losses ($200 each = $2,000). Net: -$400.

Week 3: Frustrated, he increases risk to 3% to "make it back." 6 trades. 2 wins ($600 each = $1,200), 4 losses ($300 each = $1,200). Net: $0. But the psychological damage is done.

Week 4: He takes one large trade at 5% risk to recover. Loses. Down $500 on that one trade alone.

After four weeks, he is down $700, has no data about whether his strategy actually works, and has developed a negative belief about trading. If he had spent those same four weeks testing on demo, he would have the data, the confidence, and his $10,000 still intact.

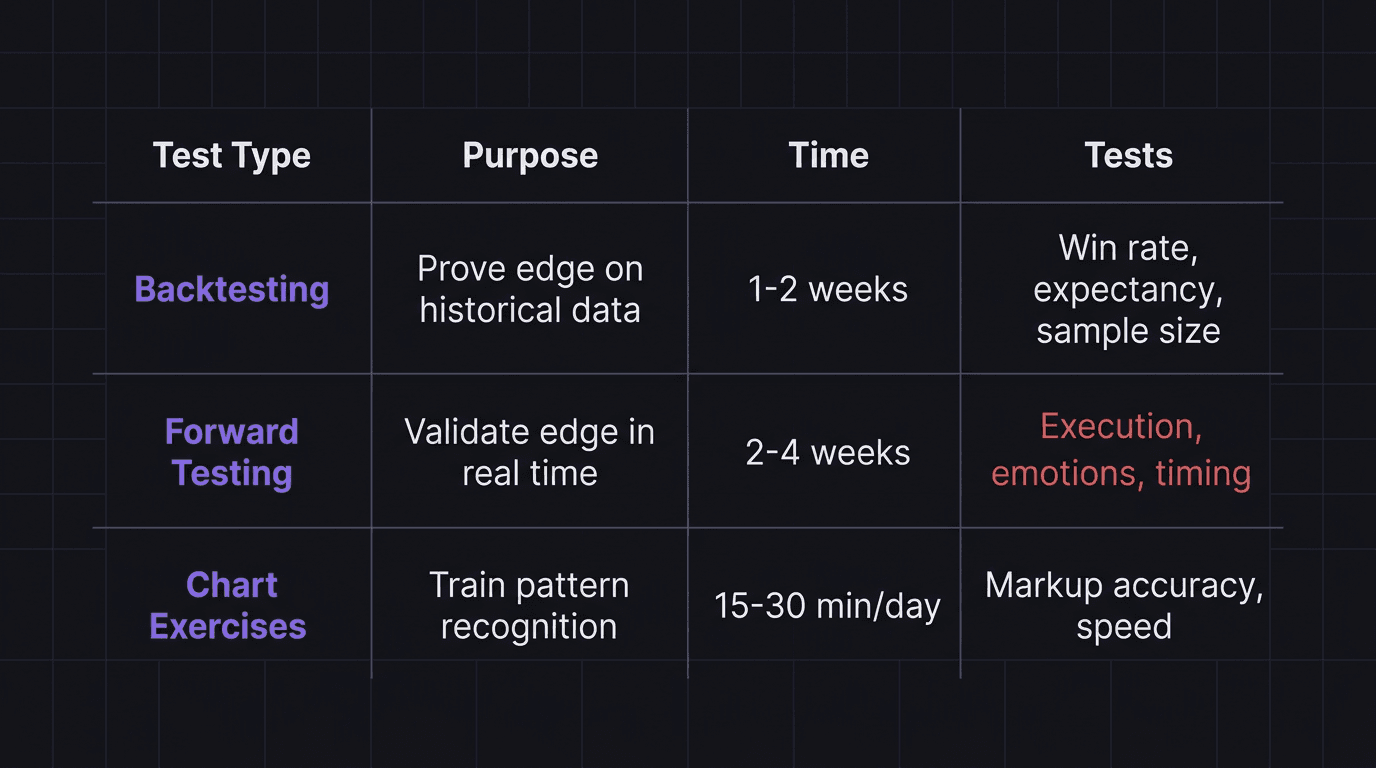

Three Types of Testing Every Trader Needs

Each testing type serves a different purpose. Doing all three gives you the most complete picture of your edge.

1. Backtesting (Historical Replay)

Backtesting means replaying historical price data and trading your strategy as if you were there live. On TradingView, you activate bar replay, which hides future candles and lets you advance one bar at a time.

What it does: Builds your initial data set. Proves the strategy has a statistical edge across a large sample size (50 to 100 trades minimum). Reveals your strategy's win rate, average R-multiple, and expectancy.

What it does not do: Test your emotional responses. In replay mode, there is no real pressure. You know you can click through 10 trades in 30 minutes, which is nothing like waiting 4 hours for a trade to play out.

Time required: 1 to 2 weeks of focused sessions (about 1 hour per day). This gives you 50 to 80 trades, depending on how many setups your strategy generates.

2. Forward Testing (Live Demo)

Forward testing means trading your strategy in real time on a demo account. You mark up your charts each morning, wait for setups to trigger during the live session, and log the results.

What it does: Validates that your backtested edge survives real market conditions. Exposes execution gaps (hesitation, missed entries, stop-moving behavior). Tests your emotional discipline under time pressure.

What it does not do: Replicate the full emotional weight of risking real money. Demo losses feel different from live losses. But forward testing catches the most common demo trading mistakes: overtrading, ignoring rules, and treating demo as consequence-free gambling.

Time required: 2 to 4 weeks of daily sessions. This gives you 20 to 40 trades, depending on your strategy's frequency.

3. Chart Exercises (Static Markup)

Chart exercises are the simplest testing type. You open a chart on a historical date, mark up the levels and zones your strategy looks for, and then scroll forward to see if price reacted as you expected. No bar replay, no demo trading. Just you, the chart, and a pen (or a screenshot tool).

What it does: Trains your pattern recognition. Makes you faster at identifying valid setups versus noise. Builds confidence in your markup accuracy.

What it does not do: Test execution or timing. You are not making real-time decisions, so it does not replace backtesting or forward testing. It supplements them.

Time required: 15 to 30 minutes per day, every day. You can do chart exercises in the evening after your forward test session. Over a month, that is 7 to 15 hours of focused pattern training.

How One Month of Testing Changes Your Results

Here is a realistic one-month testing timeline.

Week 1: Backtesting. You spend 5 sessions at 1 hour each on bar replay. You log 60 trades. Win rate: 35%. Average win: 2.8R. Average loss: 1R. Expectancy: (0.35 times 2.8) minus (0.65 times 1) = 0.98 minus 0.65 = 0.33R per trade.

Your strategy has a positive expectancy. Green light to move to forward testing.

Week 2 and 3: Forward Testing. You trade on demo daily during your chosen session (London open, for example). Over two weeks, you log 24 trades. Win rate: 33%. Average win: 2.6R. Average loss: 1.1R (slightly worse because you moved your stop on 3 trades). Expectancy: (0.33 times 2.6) minus (0.67 times 1.1) = 0.858 minus 0.737 = 0.12R per trade.

Still positive, but lower than your backtest. The gap is the 3 trades where you moved your stop. You identify the pattern in your journal: you moved stops after two consecutive losses. That behavioral fix becomes your focus for week 3 and 4.

Week 3 and 4: Forward Testing + Chart Exercises. You continue forward testing but add 20 minutes of chart exercises each evening. You log another 22 forward test trades. Win rate: 36%. Average loss back to 1R because you stopped moving your stop. Expectancy climbs back to 0.28R.

60 backtested trades showing positive expectancy

46 forward tested trades confirming the edge holds in real time

A clear behavioral fix (stop-moving) identified and corrected through journaling

20+ hours of chart exercise training sharpening your pattern recognition

Compare that to the trader who skipped testing and went live on day one. You have the same strategy, but you also have the data, the practice, and the self-knowledge. That is the difference between guessing and trading.

What Your Test Data Should Show Before Going Live

Do not go live until your data passes these checkpoints:

Positive expectancy across both testing phases. Your expectancy must be positive in your backtest AND your forward test. If your backtest is positive but your forward test is negative, you have an execution problem, not a strategy problem.

Consistent win rate. Your forward test win rate should be within 5 to 10 percentage points of your backtest win rate. A backtest at 35% and a forward test at 30% is fine. A backtest at 35% and a forward test at 15% is a red flag.

Adequate sample size. At minimum, 50 trades across backtesting and forward testing combined. Ideally 80 or more. With fewer trades, your numbers are noise, not signal. Check your sample size requirements before making any conclusions.

Rule adherence above 80%. If fewer than 80% of your trades followed your plan exactly, your data is contaminated. The results reflect a mix of your strategy and your impulses. Fix the rule-breaking, retest, and get clean data.

Survivable worst streak. Your backtest will show your longest losing streak. Can your account survive it? Can your psychology handle it? If your worst streak was 7 losses and you know you start tilting after 3, you have a problem to solve before going live.

Walkthrough: Ready vs. Not Ready

Ready: 65 backtested trades (37% win rate, 0.35R expectancy). 35 forward tested trades (34% win rate, 0.28R expectancy). Rule adherence: 87%. Worst streak: 6 losses. Behavioral fix identified and corrected mid-test. Account would survive the worst streak with 0.5% risk at minimum.

Not ready: 30 backtested trades (42% win rate, 0.50R expectancy, but sample is too small). 12 forward tested trades (25% win rate, negative expectancy). Rule adherence: 60%. Worst streak: 5 losses, but the trader increased risk after each one.

The numbers tell the story. The first trader has proof. The second has hope. Only one of them should be trading with real money.

How EdgeFlo Keeps Your Testing Phase Organized

Testing generates a lot of data across multiple phases, and losing track of it defeats the purpose. EdgeFlo's journal lets you tag every trade by testing phase (backtest, forward test, or live), so your data stays clean and comparable. The dashboard calculates expectancy for each phase separately, letting you see at a glance whether your forward test matches your backtest.

The Edge plan builder stores your strategy rules in one place, visible during every session. When you are forward testing and a setup appears, your plan is right there. No guessing whether this trade meets your criteria. No rationalizing a bad entry because you forgot a rule.

After the testing month is done and your data is solid, transitioning to live trading inside EdgeFlo is seamless. Your journal, dashboard, and plan carry forward. The only thing that changes is the account type. And that continuity is what keeps the discipline you built during testing alive when real money enters the picture.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

Why do I need a full month of testing before live trading?

What are chart exercises in trading?

Can I test on a live account with small size instead of demo?

What numbers should I see before going live?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.