Forward Testing: From Backtest to Live Without Gambling

Forward testing bridges backtesting and live trading. Learn how to paper trade a strategy in real-time conditions and know when you're ready for real capital.

Forward testing is the step between backtesting and live trading where you run your strategy in real-time market conditions without risking real money. It proves whether you can actually execute a plan under pressure, not just whether the plan looked good on a historical chart. Most traders skip it entirely, jump to live capital, and wonder why their "proven" strategy falls apart. This article walks you through exactly how to forward test properly, what data to track, and how to know when you're genuinely ready for real money.

TL;DR

Backtesting tells you if a strategy works on paper. Forward testing tells you if you can work the strategy in real time.

Paper trade a minimum of 30 setups with the same rules, tracking win rate, average R, and profit factor.

Forward testing exposes real-world problems backtesting hides: slippage, hesitation, spreads, and emotional decision-making.

You are ready for live trading when your forward test results match your backtest results within a reasonable margin over 30+ trades.

Track both phases in the same journal so you can compare test data against live data side by side.

Why Backtesting Alone Isn't Enough

If you have already run a backtesting trading strategy and it looked profitable, you are ahead of most traders. But here is the problem: backtesting gives you the luxury of hindsight. You already know what happened. You see the full candle, the reaction, the outcome. There is no uncertainty, no adrenaline, no second-guessing.

In real-time markets, you do not get that comfort. You see price approaching your level and you have to decide right now. Is this the setup? Do I enter? Where is my stop? Your backtest said this works 58% of the time, but your hands are hovering over the keyboard and the candle is moving fast.

Sound familiar?

Backtesting also cannot account for a few things that matter a lot in live conditions:

Slippage. Your entry fills 2 pips worse than planned. Over 30 trades, that changes your R:R.

Spreads. They widen during news events. Your backtest used fixed spreads. Reality does not.

Hesitation. You see the setup, freeze for 10 seconds, and the entry is gone. This never happens in a backtest.

Overtrading. You take setups that "almost" match your rules because you are bored or want to make up a loss.

Professional traders collect data, analyze their edge, and refine their execution before putting real money on the line. Forward testing is where that refinement happens.

What Forward Testing Actually Proves

Forward testing (also called paper trading) is when you take your strategy and test it in live market conditions without risking real capital. You watch real charts, in real time, and make real decisions. The only thing missing is money on the line.

This is not a watered-down version of trading. It is a data collection phase. You are answering one specific question: does my execution match my backtest?

Here is what forward testing actually reveals:

Your real win rate under pressure. Backtesting might show 60%. Forward testing might show 48% because you hesitate on entries or exit early when price stalls. That gap is the gap between your plan and your execution.

Your actual R:R after slippage. If your backtest assumed clean 2R winners, but your forward test entries keep filling 1-3 pips late, your realized R:R is closer to 1.7R. That matters.

Your discipline patterns. Do you follow your rules on trade 1 through 10, then start improvising on trade 11? Forward testing exposes where your discipline breaks down. A trading review process after each session catches these patterns before they cost you money.

Your trading edge in current conditions. A strategy that worked on 2024 data might not work in March 2026. Forward testing proves it works right now, in the market you are actually going to trade.

Back testing helps you see if your trading system works. Forward testing gives you the confidence to work the system without fear.

How to Forward Test Without Wasting Months

The biggest complaint about forward testing is that it takes too long. Traders want to get to live capital. They paper trade for three days, feel "ready," and fund an account.

That is not forward testing. That is impatience wearing a process hat.

Here is how to do it efficiently without burning months.

The 30-Trade Minimum

Thirty trades is the practical floor for a useful sample. Fewer than that and one lucky streak or one bad week can distort everything. At 30 trades, statistical noise smooths out enough to see real patterns.

If you trade one setup per day, that is roughly six weeks. If you trade intraday and take 2-3 setups per session, you can reach 30 in two to three weeks.

Track Everything in a Journal

Every forward test trade goes in your trading journal template with the same detail you would use for a live trade. No shortcuts because "it is just paper."

For each trade, record:

Date and session (London, New York, overlap)

Pair and timeframe

Setup type (the exact pattern from your rules)

Entry, stop loss, and target prices

Planned R:R

Result (win, loss, breakeven)

Realized R (actual, including any slippage)

Notes (did you follow your rules? any hesitation? anything unusual?)

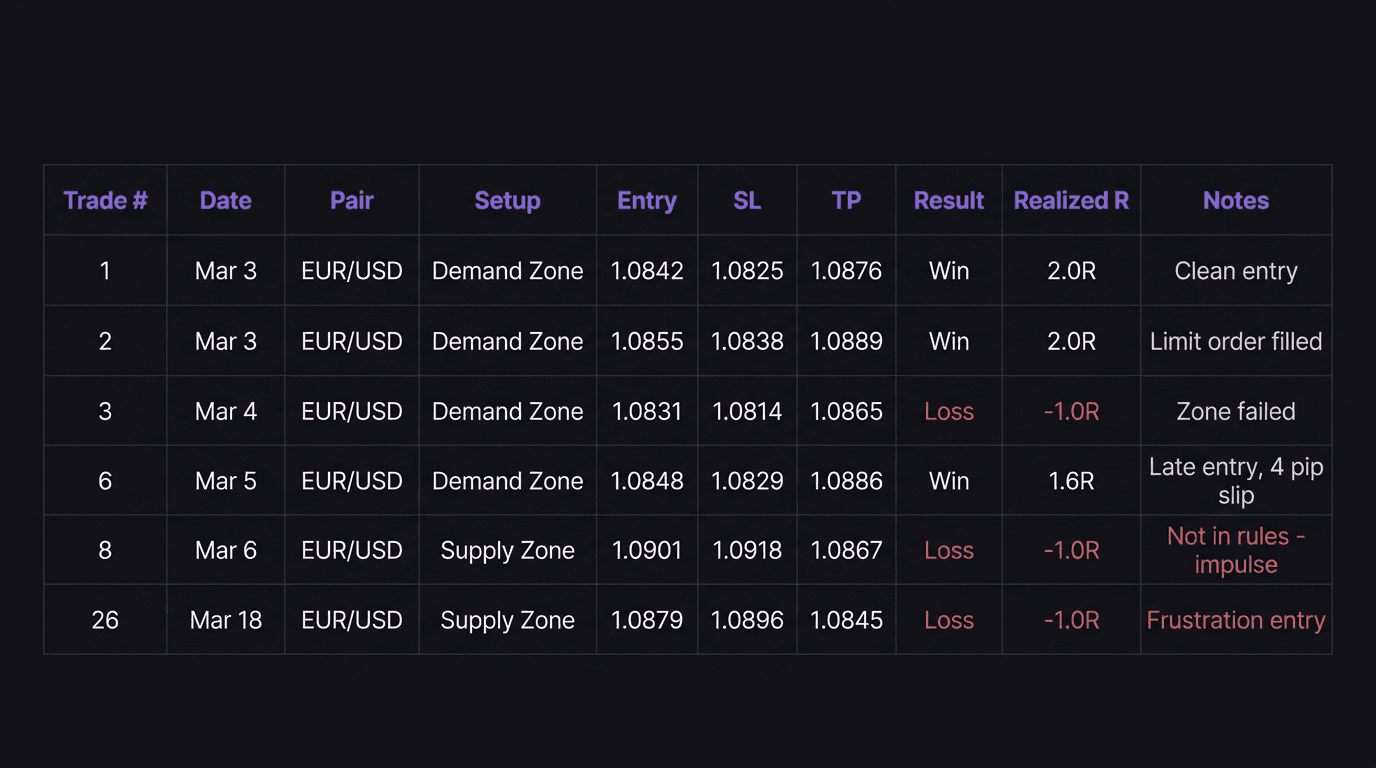

Walkthrough: Paper Trading a Supply/Demand Setup for 30 Trades

The setup: A trader has backtested a supply and demand strategy on EUR/USD 1-hour charts. The backtest showed a 55% win rate with an average 2R reward. Now they forward test it.

Week 1 (Trades 1-8): The trader identifies demand zones during the Asian session and sets alerts for London open. Trades 1-5 go well: three wins, two losses, all following the rules. But on trade 6, price approaches the zone and the trader hesitates. By the time they place the order, the entry is 4 pips worse. The trade hits target, but realized R is 1.6 instead of 2.0. Trade 7 is a valid setup the trader skips entirely because the previous trade felt uncomfortable. Trade 8 is a revenge entry on a zone that does not meet the criteria.

Week 2 (Trades 9-18): After reviewing the first week through a post-trade review, the trader notices two problems: hesitation on entries and one impulsive trade. They add a rule: set limit orders at the zone edge instead of entering manually. This removes the hesitation problem. Trades 9-18 are cleaner. Win rate so far: 11 wins out of 18 trades (61%). Average realized R: 1.8.

Week 3-4 (Trades 19-30): The trader hits a four-trade losing streak (trades 22-25). This is normal variance but it triggers frustration. Trade 26 is another impulse entry outside the rules. After reviewing, they tag the impulse trade separately. Final 30-trade results: 17 wins, 13 losses (56.7% win rate). Average winner: 1.85R. Average loser: 1.0R. Profit factor: 1.62.

The comparison: Backtest said 55% win rate, 2.0R average. Forward test showed 56.7% win rate but 1.85R average (slippage and one early exit). Profit factor is positive. The edge is real, but execution needs a small adjustment: limit orders instead of market orders. Two rule-breaking trades were tagged and excluded from the final calculation.

That is the entire process. No magic. Just data.

What "Good Enough" Looks Like

Your forward test does not need to beat your backtest. It needs to be in the same ballpark. If your backtest showed a 55% win rate and your forward test shows 52%, that is fine. The edge is intact. If your backtest showed 55% and your forward test shows 38%, something is breaking in your execution.

The numbers to compare:

Metric | What to Compare |

|---|---|

Win rate | Forward test within 5-8% of backtest |

Average R per winner | Should not drop more than 0.3R from backtest |

Profit factor | Must stay above 1.0 (ideally above 1.3) |

Rule-following rate | Percentage of trades that matched your exact criteria |

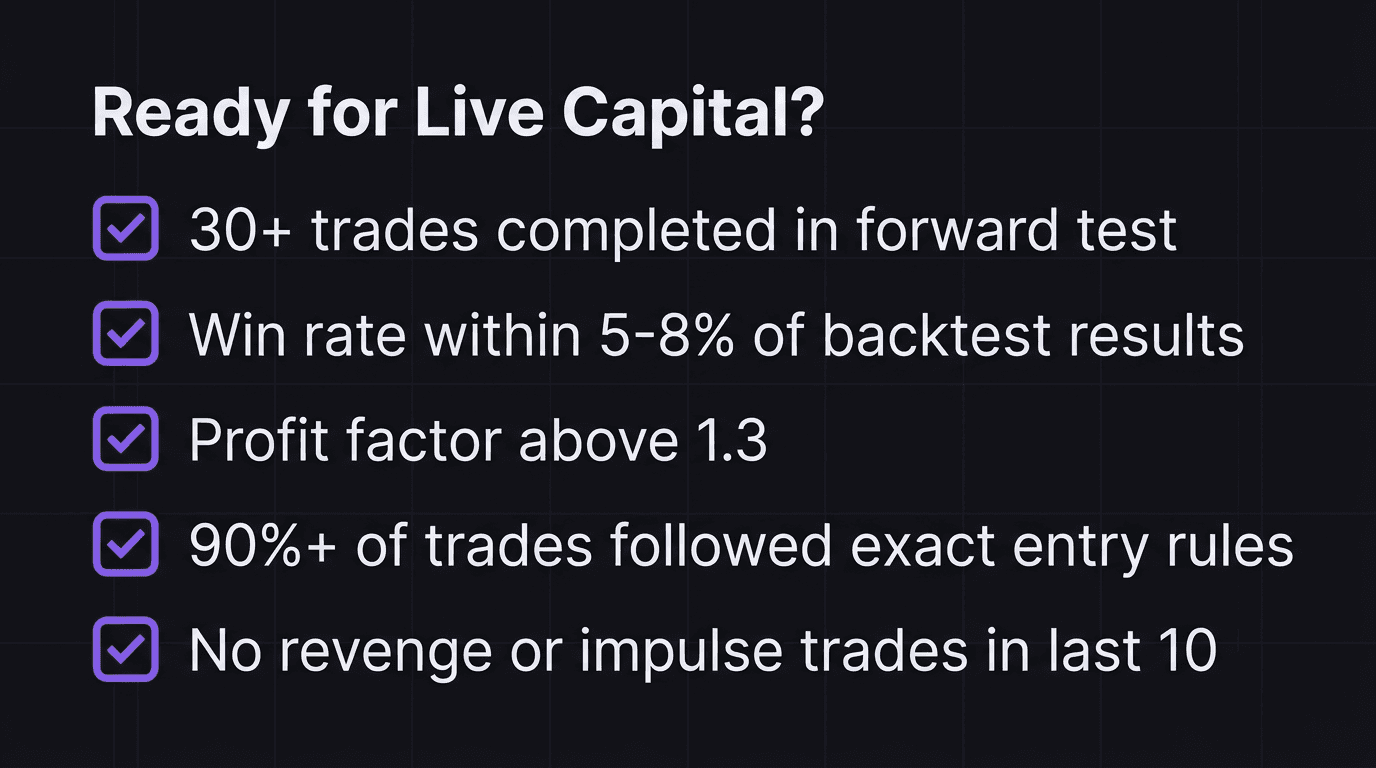

When You're Ready for Live (The Checklist)

Not every completed forward test means you are ready. Here is the honest checklist.

1. You have 30+ forward test trades logged. Not 12. Not "about 20." Thirty minimum, documented with entries, exits, and notes.

2. Your win rate is within range of your backtest. A 5-8% drop is normal (execution friction). A 15%+ drop means something is wrong.

3. Your profit factor is above 1.3. A profit factor of 1.0 means you break even before commissions. Below 1.3 and commissions will eat your edge.

4. At least 90% of your trades followed your exact rules. If you broke rules on 5 out of 30 trades, that is 17% improvisation. Fix the discipline problem before adding real money to it.

5. No revenge or impulse trades in your last 10. The last 10 trades are a window into your current state. If they are clean, your process is stable. If trade 28 was an impulse entry, you are not there yet.

What If You Fail the Checklist?

Go back. Not to the beginning. Just address the specific gap.

If your win rate is off, review your entries. Are you hesitating? Taking setups that do not meet your criteria? Your trading review process should identify the exact trades where execution broke down.

If discipline is the problem, that is not a strategy issue. That is a behavior issue. Forward test another 15-20 trades with one focus: follow the rules every single time, regardless of outcome.

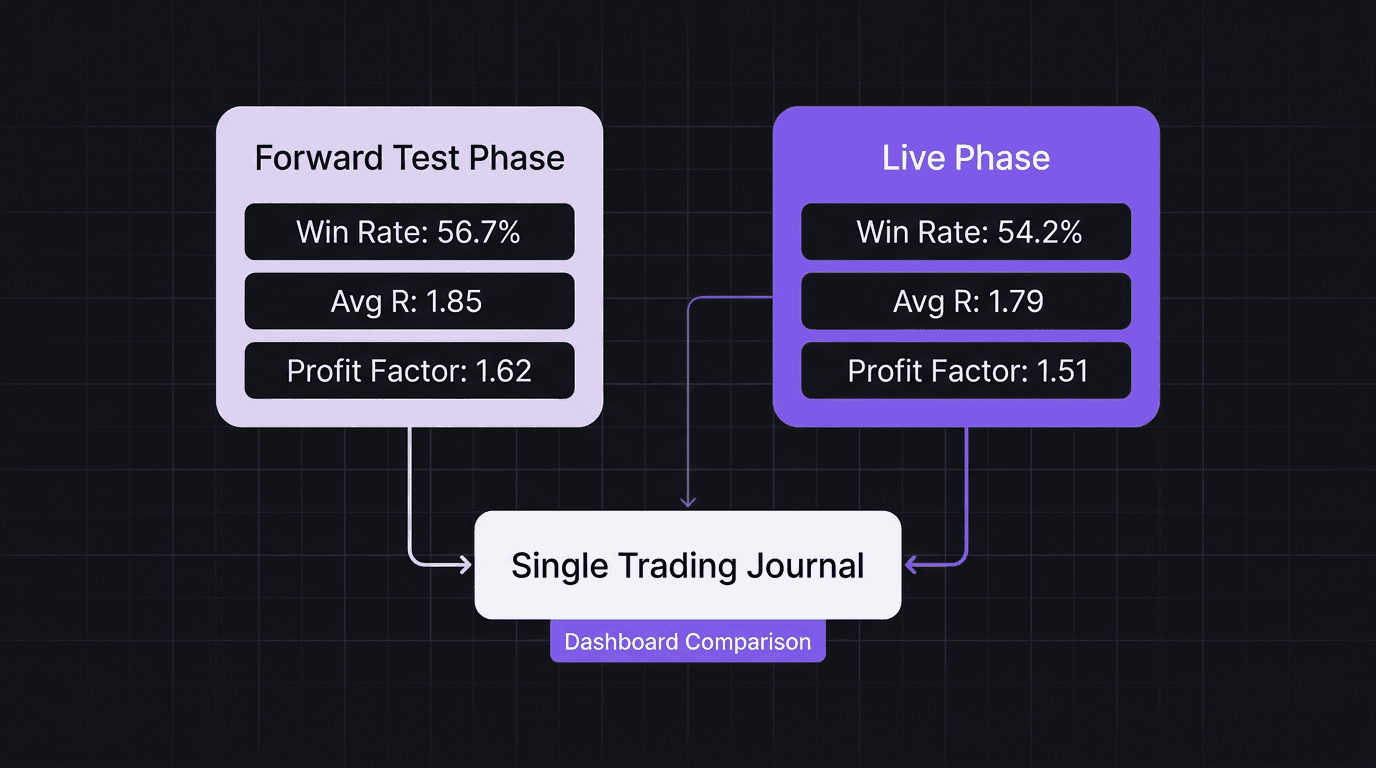

How EdgeFlo Tracks Your Forward Test Results

Tracking forward test trades in a spreadsheet works, but it falls apart when you transition to live. You end up with data in two places, different formats, and no easy way to compare phases.

EdgeFlo's trading journal tracks performance data across both test and live phases in the same place. Every trade gets logged with the same fields whether you are paper trading or using real capital. When you flip to live, your historical forward test data is already there for comparison.

The dashboard shows win rate and profit factor over time, so you can see exactly when your execution started matching your backtest. Instead of eyeballing a spreadsheet and hoping the numbers add up, you get a clear visual of whether your edge held through the forward test and whether it is holding in live conditions.

That single-source tracking is the difference between guessing you are ready and knowing it. Your forward test results sit right next to your live results. If performance drops after going live, you can pinpoint exactly which metric shifted and trace it back to specific trades.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

How many forward test trades do I need before going live?

Can I forward test on a demo account instead of paper trading?

What is the difference between forward testing and backtesting?

Should I forward test every new strategy before trading it live?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.