Trading Expectancy: The Metric That Predicts Profitability

Trading expectancy reveals if your strategy makes money over time. Learn the formula, calculate your own, and see why win rate alone means nothing.

Trading expectancy is a single number that tells you whether your strategy will make or lose money over a large sample of trades. It combines your win rate, average win size, and average loss size into one metric. If the number is positive, your strategy has an edge. If it is negative, you are bleeding money on every trade you take, even if some of those trades are winners.

Most traders obsess over win rate. But win rate alone is meaningless without knowing how much you win when you are right and how much you lose when you are wrong.

TL;DR

Trading expectancy measures how much you gain (or lose) per dollar risked, on average.

A strategy with a 30% win rate can be profitable if the reward-to-risk ratio is high enough.

The formula: (Win Rate x Avg Win) - (Loss Rate x Avg Loss) = Expectancy per trade.

You need at least 30 trades (ideally 100+) to get a reliable expectancy number.

A positive expectancy only works if you pair it with consistent position sizing.

Why a 30% Win Rate Can Be Profitable

Here is the thing that trips up most traders: you do not need to be right most of the time to make money. Trading is a probability game. It is not about how many trades you win or lose. It is about how much you make when you are right and how much you lose when you are wrong.

Picture a trader who loses 7 out of every 10 trades. Sounds terrible, right? But what if each loss is $100 and each win is $350?

7 losses: 7 x $100 = $700 lost

3 wins: 3 x $350 = $1,050 gained

Net profit: $350

That is a 30% win rate producing a $350 profit on 10 trades. The math works because the average win is 3.5 times larger than the average loss.

Now flip it. A trader with an 80% win rate sounds great. But if they make $50 on winners and lose $300 on losers:

8 wins: 8 x $50 = $400 gained

2 losses: 2 x $300 = $600 lost

Net loss: -$200

An 80% win rate, and still losing money. This is why win rate alone tells you nothing. You need the full picture, and that full picture is expectancy.

The Expectancy Formula (With Real Numbers)

The formula is straightforward:

Expectancy = (Win Rate x Average Win) - (Loss Rate x Average Loss)

Where Loss Rate = 1 - Win Rate.

You can also express this per dollar risked:

Expectancy per $1 risked = (Win Rate x Avg Reward-to-Risk) - (Loss Rate x 1)

The second version is useful when you want to compare strategies that use different position sizes. It normalizes everything to a single dollar of risk.

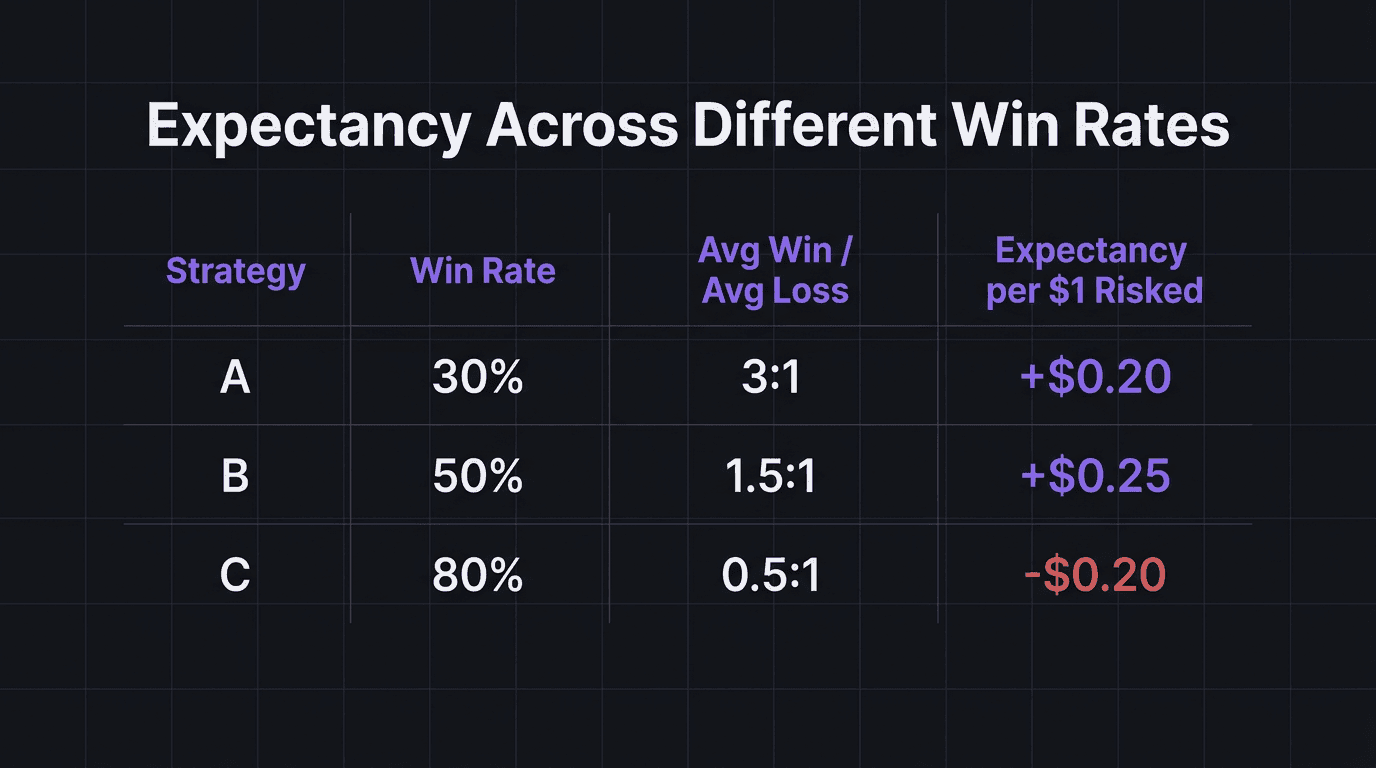

Example: The 30% Win Rate Strategy

Win Rate: 30% (0.30)

Loss Rate: 70% (0.70)

Average Win: $300 (3R)

Average Loss: $100 (1R)

Expectancy per trade = (0.30 x $300) - (0.70 x $100) Expectancy per trade = $90 - $70 Expectancy per trade = $20

Per dollar risked = (0.30 x 3) - (0.70 x 1) = 0.90 - 0.70 = $0.20 per $1 risked

Every time you risk $1, you expect to make $0.20 on average. Over 100 trades risking $100 each, that is $2,000 in expected profit. But you need to survive the losing streaks to get there, which is where position sizing becomes critical.

Double-Checking Strategy B

Win Rate: 50% (0.50), Loss Rate: 50% (0.50)

Avg Win: $150 (1.5R), Avg Loss: $100 (1R)

Expectancy = (0.50 x $150) - (0.50 x $100) = $75 - $50 = $25 per trade

Per $1 risked = (0.50 x 1.5) - (0.50 x 1) = 0.75 - 0.50 = $0.25

Double-Checking Strategy C

Win Rate: 80% (0.80), Loss Rate: 20% (0.20)

Avg Win: $50 (0.5R), Avg Loss: $100 (1R)

Expectancy = (0.80 x $50) - (0.20 x $100) = $40 - $20 = $20 per trade

Per $1 risked = (0.80 x 0.5) - (0.20 x 1) = 0.40 - 0.20 = $0.20

Wait. Strategy C actually has a positive expectancy of $0.20 per dollar risked? Yes. But here is the catch: in reality, traders with high win rates and small wins tend to let their losers run far beyond the planned stop. The average loss balloons. If those two losses per ten trades become $250 each instead of $100, the math collapses:

Adjusted: (0.80 x $50) - (0.20 x $250) = $40 - $50 = -$10 per trade

That is why you need to track your actual numbers, not your planned ones. Your equity curve will show the truth long before the spreadsheet does.

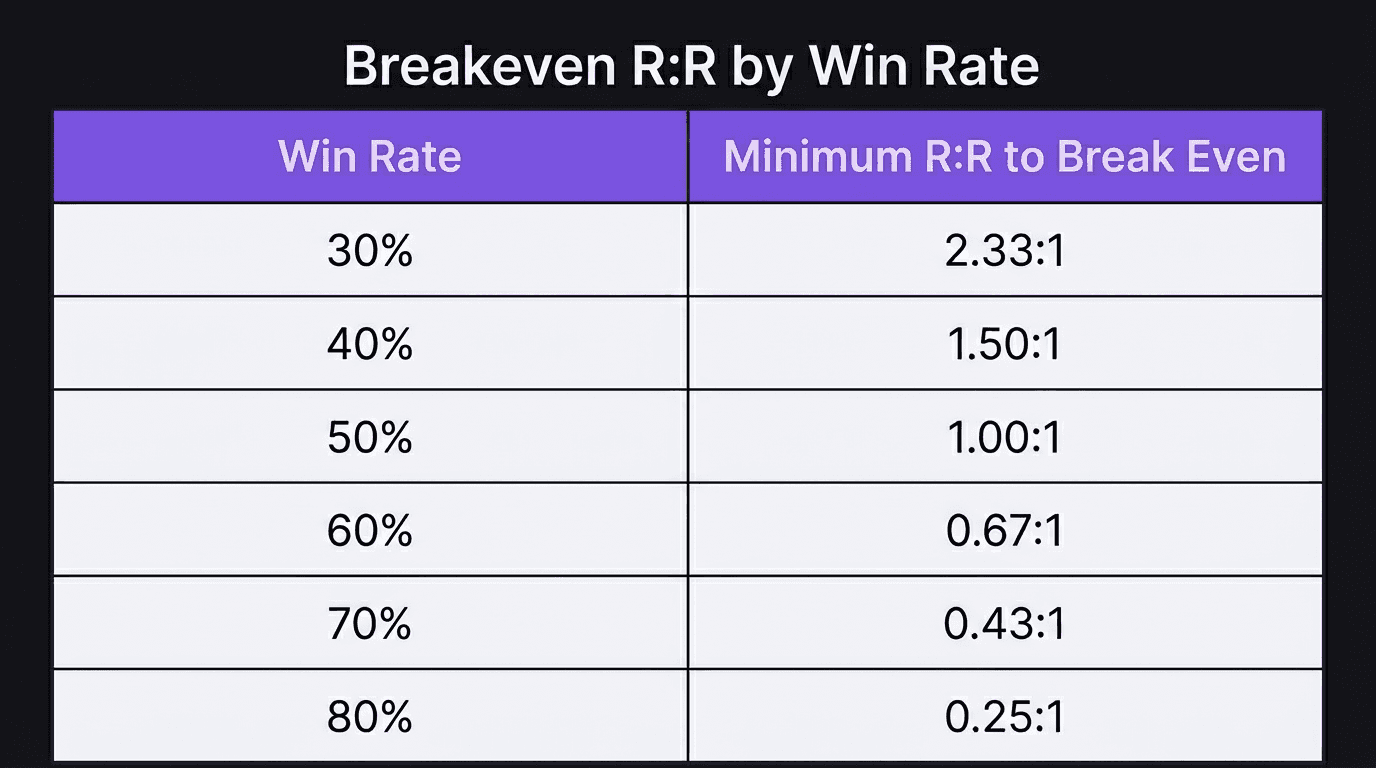

Win Rate vs Reward-to-Risk: Finding the Balance

There is no "best" win rate. There is only the right combination of win rate and reward-to-risk that gives you positive expectancy.

Here is the breakeven line. Any combination above it is profitable:

Win Rate | Minimum R:R to Break Even |

|---|---|

30% | 2.33:1 |

40% | 1.50:1 |

50% | 1.00:1 |

60% | 0.67:1 |

70% | 0.43:1 |

80% | 0.25:1 |

The math: Breakeven R:R = (1 - Win Rate) / Win Rate. At 30% win rate, that is 0.70 / 0.30 = 2.33. Anything above 2.33:1 with a 30% win rate and you are profitable.

Sound familiar? You can have a strategy that wins only three out of ten times and still be making money, as long as your winners are big enough. Your edge does not guarantee you will win any single trade. It just improves your odds over a large sample.

The real question is not "what win rate should I aim for?" It is "what expectancy does my actual trading produce?" That answer comes from your journal and your trading performance review, not from theoretical setups.

Walkthrough: Calculating Your Own Expectancy

Grab your last 50 trades. Here is how to calculate your expectancy step by step.

Step 1: Count Wins and Losses

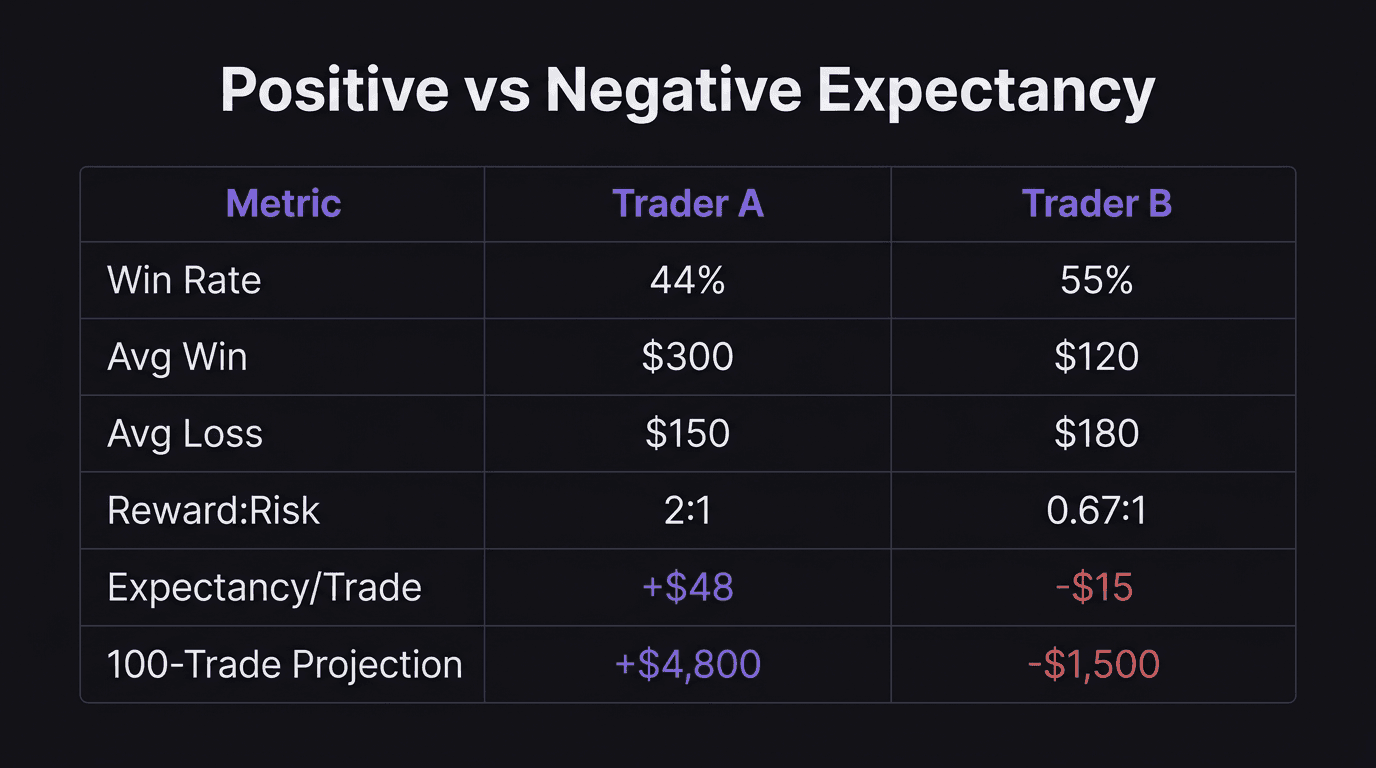

Say you have 50 trades. 22 were winners, 28 were losers.

Win Rate = 22 / 50 = 0.44 (44%)

Loss Rate = 28 / 50 = 0.56 (56%)

Step 2: Calculate Average Win and Average Loss

Add up all your winning trade profits and divide by the number of wins. Do the same for losses.

Total profit from winners: $6,600

Average Win: $6,600 / 22 = $300

Total loss from losers: $4,200

Average Loss: $4,200 / 28 = $150

Step 3: Plug Into the Formula

Expectancy = (Win Rate x Avg Win) - (Loss Rate x Avg Loss) Expectancy = (0.44 x $300) - (0.56 x $150) Expectancy = $132 - $84 Expectancy = $48 per trade

Over your next 100 trades (assuming the same edge holds), you would expect roughly 100 x $48 = $4,800 in profit.

Step 4: Express Per Dollar Risked

If your average loss is $150, that is your risk per trade.

Expectancy per $1 risked = $48 / $150 = $0.32 per $1 risked

For every dollar you put at risk, you expect to make $0.32 back. That is a solid edge.

What a Negative Result Looks Like

Same exercise, different numbers. A trader with 55% win rate, $120 average win, $180 average loss:

Expectancy = (0.55 x $120) - (0.45 x $180) Expectancy = $66 - $81 Expectancy = -$15 per trade

A 55% win rate and still losing money. This trader is right more often than wrong and still going broke. Without running this calculation, they might keep trading the same way for months, wondering why the account keeps shrinking. This is exactly why a regular trading performance review matters more than checking your P&L after every session.

If you have a 60% win rate over 500 trades, you will not freak out if you lose five in a row. You know that over large numbers, the edge plays out. But if you have never calculated your expectancy, five losses in a row feels like the strategy is broken. It probably is not. You just do not have the data to prove it yet.

The fix is straightforward: backtest your trading strategy across enough trades to trust the number, then track it in real-time as you execute.

How EdgeFlo Calculates Expectancy for You

Running this math by hand every week gets old fast. And most traders simply do not do it, which means they trade blind.

EdgeFlo's trading dashboard surfaces your win rate, average R, and profit factor automatically. You do not need a spreadsheet. Every trade you log feeds into these metrics in real time, so your expectancy stays current as your trading evolves. The data acts as a mirror: it shows whether your edge is positive or whether something has shifted.

When your expectancy drifts negative, the dashboard makes it visible before your account balance does. That early signal gives you the chance to pause, review, and adjust, instead of discovering the problem after a drawdown that takes weeks to recover from.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

What is a good trading expectancy?

Can you have a low win rate and still be profitable?

How many trades do I need to calculate expectancy?

Is trading expectancy the same as expected value?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.