Position Sizing Across Markets: Forex, Futures, and Stocks

Position sizing rules change by market. Learn how to apply 1% risk per trade across forex lots, futures contracts, and stock shares with concrete examples.

Risk 1% per trade. You have heard that rule a hundred times. But "1% risk" means different things depending on whether you are sizing a forex position in lots, a futures contract in ticks, or a stock position in shares.

The principle is identical across every market: calculate your dollar risk first, then work backward to the correct position size using that market's specific unit of measurement. The math changes. The discipline does not.

Most traders who blow up in a new market do not blow up because of bad entries. They blow up because they sized their position using the wrong math for that instrument. A 1-lot position in EUR/USD risks $10 per pip. A 1-contract position in NQ risks $5 per tick. Using forex intuition to size a futures trade will get you hurt.

TL;DR

Position sizing starts the same everywhere: dollar risk = account size times risk percentage.

Forex sizing uses lots and pip value. Futures sizing uses contracts and tick value. Stocks sizing uses shares and per-share risk.

The most common sizing mistake is carrying one market's intuition into a different market's math.

Use 1% risk as your default across all markets until you have 100+ trades proving you can handle more.

Automate the calculation to remove mental math errors under pressure.

Why Position Sizing Rules Change by Market

Position sizing always starts from the same place: how much money are you willing to lose on this trade?

If your account is $100,000 and you risk 1% per trade, your dollar risk is $1,000. That number stays the same whether you trade EUR/USD, NQ futures, or Tesla stock.

What changes is how you convert that $1,000 into a position size. Each market has its own unit of measurement for price movement, and each unit has its own dollar value:

Forex: Price moves in pips. Each pip has a dollar value that depends on the pair and your lot size. For EUR/USD, 1 standard lot = $10 per pip.

Futures: Price moves in ticks. Each tick has a fixed dollar value set by the exchange. For NQ (Nasdaq 100 E-mini), 1 contract = $5 per tick.

Stocks: Price moves in dollars per share. If you own 100 shares and the stock drops $1, you lose $100.

The mistake is assuming that "1 lot" in forex and "1 contract" in futures carry similar risk. They do not. And mixing up the math is how a controlled 1% risk trade becomes a 3% or 4% surprise loss.

Forex: Lots, Pips, and Dollar Risk

Forex position sizing uses this formula:

Position size (lots) = Dollar risk / (Stop distance in pips x Pip value per lot)

Forex lot sizes come in three tiers: standard (1.0 lot), mini (0.1 lot), and micro (0.01 lot). The pip value scales with the lot size.

1 standard lot = $10 per pip

1 mini lot = $1 per pip

1 micro lot = $0.10 per pip

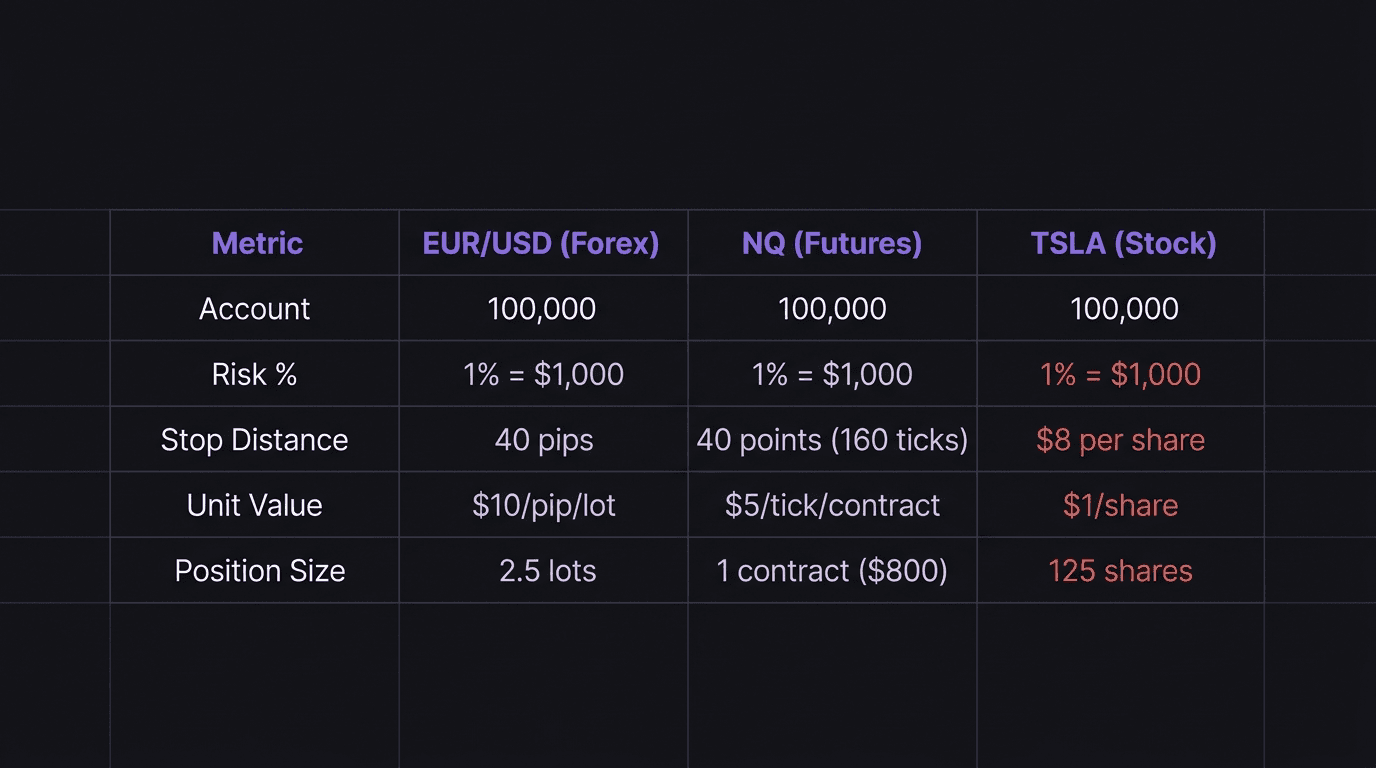

Walkthrough: EUR/USD at 1% Risk

Account: $100,000. Risk: 1% = $1,000. Pair: EUR/USD. Stop: 40 pips.

Position size = $1,000 / (40 pips x $10 per pip) = $1,000 / $400 = 2.5 lots.

Math check: - Dollar risk per pip: 2.5 lots x $10 = $25 per pip. - $25 per pip x 40 pips = $1,000. - $1,000 / $100,000 = 1%. Confirmed.

If the stop was 25 pips instead: $1,000 / (25 x $10) = $1,000 / $250 = 4.0 lots.

Math check: - 4.0 lots x $10 = $40 per pip. - $40 x 25 pips = $1,000. - $1,000 / $100,000 = 1%. Confirmed.

Notice that the lot size changes based on the stop distance, not based on how confident you feel. Wider stop = smaller position. Tighter stop = larger position. The dollar risk stays fixed at $1,000 either way.

For JPY pairs (USD/JPY, EUR/JPY, GBP/JPY), the pip value is approximately $6.60 per pip per standard lot (it varies slightly with the exchange rate). The formula stays the same, but you plug in $6.60 instead of $10.

Futures: Contracts and Tick Value

Futures sizing uses this formula:

Number of contracts = Dollar risk / (Stop distance in ticks x Tick value per contract)

The critical difference from forex: futures contracts come in fixed sizes. You cannot trade 2.5 contracts. You trade 1, 2, 3, or more. This means your actual risk will rarely match your target risk exactly.

NQ (Nasdaq 100 E-mini): 1 tick = $5.00 per contract. Minimum tick = 0.25 points, so 1 point = 4 ticks = $20 per contract.

ES (S&P 500 E-mini): 1 tick = $12.50 per contract. Minimum tick = 0.25 points, so 1 point = 4 ticks = $50 per contract.

MNQ (Micro Nasdaq): 1 tick = $0.50 per contract. Same tick structure as NQ but at 1/10th the size.

Walkthrough: NQ Futures at 1% Risk

Account: $100,000. Risk: 1% = $1,000. Stop: 40 points on NQ (160 ticks).

Dollar risk per contract at 40 points: 160 ticks x $5 = $800 per contract.

Number of contracts: $1,000 / $800 = 1.25 contracts.

Since you cannot trade 1.25 contracts, you round down to 1 contract.

Actual risk at 1 contract: 160 ticks x $5 = $800 = 0.8% of account.

Math check: - 160 ticks x $5 per tick = $800. - $800 / $100,000 = 0.8%.

If you rounded up to 2 contracts: 160 ticks x $5 x 2 = $1,600 = 1.6% risk. That is 60% more than your target. On a funded account with a daily loss limit of 5%, two bad trades at 1.6% each puts you at 3.2% drawdown. Rounding up is how funded traders fail.

The fix: Use MNQ (Micro Nasdaq) for finer sizing. At $0.50 per tick, the same 40-point stop costs $80 per contract. $1,000 / $80 = 12.5 contracts, round to 12 or 13. Much closer to your target 1%.

Stocks: Shares and Per-Share Risk

Stock sizing is the most intuitive:

Number of shares = Dollar risk / Stop distance in dollars per share

If you buy a stock at $200 and place your stop at $192, your per-share risk is $8. With $1,000 dollar risk, you buy 125 shares.

Walkthrough: Stock Trade at 1% Risk

Account: $100,000. Risk: 1% = $1,000. Stock: TSLA at $200. Stop: $192 (risk of $8 per share).

Number of shares: $1,000 / $8 = 125 shares.

Total position value: 125 x $200 = $25,000 (25% of account value). This is important. Your risk is 1%, but your position value is 25% of your account. These are different numbers, and confusing them is a common mistake.

Math check: - 125 shares x $8 per share risk = $1,000. - $1,000 / $100,000 = 1%. Confirmed.

If the stop was wider at $185 ($15 per share risk): $1,000 / $15 = 66 shares.

Math check: - 66 shares x $15 = $990. - $990 / $100,000 = 0.99%. Close enough.

The principle is identical to forex and futures: wider stops reduce your position size, tighter stops increase it. The dollar risk stays fixed.

One stock-specific trap: gap risk. If a stock closes at $200 and opens the next day at $185 due to after-hours news, your $8 per share stop at $192 never triggers. You take a $15 per share loss instead of $8. This is why stock traders often use smaller risk percentages or avoid holding through earnings announcements. Risk-reward ratios need to account for gap risk in stocks more than in forex, where gaps are rare outside of weekend holds.

How EdgeFlo Calculates Size for Any Market

The auto lot size calculator in EdgeFlo adapts to forex, futures, and stocks. Enter your stop-loss level, and the calculator outputs the correct position size based on your account balance and risk percentage. No switching between spreadsheets. No manual pip-to-dollar conversions. No rounding errors from doing mental math during a fast-moving session.

For forex, it calculates lots based on the pair's pip value. For futures, it uses the contract's tick value and rounds to the nearest tradeable contract size (showing you the actual risk percentage after rounding). For stocks, it divides dollar risk by per-share risk.

The value is not just convenience. It is error prevention. When NQ is moving 20 points in a minute and you need to size a position, the difference between 1 contract and 2 contracts is the difference between 0.8% risk and 1.6% risk. That is not a rounding error. That is a risk management failure. Automating the calculation removes the one step where most multi-market traders make their most expensive mistake.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

Does 1% risk mean the same thing in forex and futures?

Why is futures position sizing harder than forex?

Can I use the same risk percentage across all markets?

What happens if I size based on dollars instead of percentages?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.