Institutional vs Retail Trading: The Liquidity Gap

Retail traders fill orders instantly. Institutions need millions in counterparty orders. Learn why this liquidity gap drives price manipulation and how to align with smart money.

A retail trader placing a $10,000 order never thinks about counterparties. The order fills in milliseconds. No friction. No price impact. But an institutional trader placing a $50 million order faces a completely different problem: there are not enough sellers at one price to absorb that size. This gap between how retail and institutional orders fill is the reason liquidity sweeps exist, why "manipulation" feels real, and why understanding the difference changes how you read every chart.

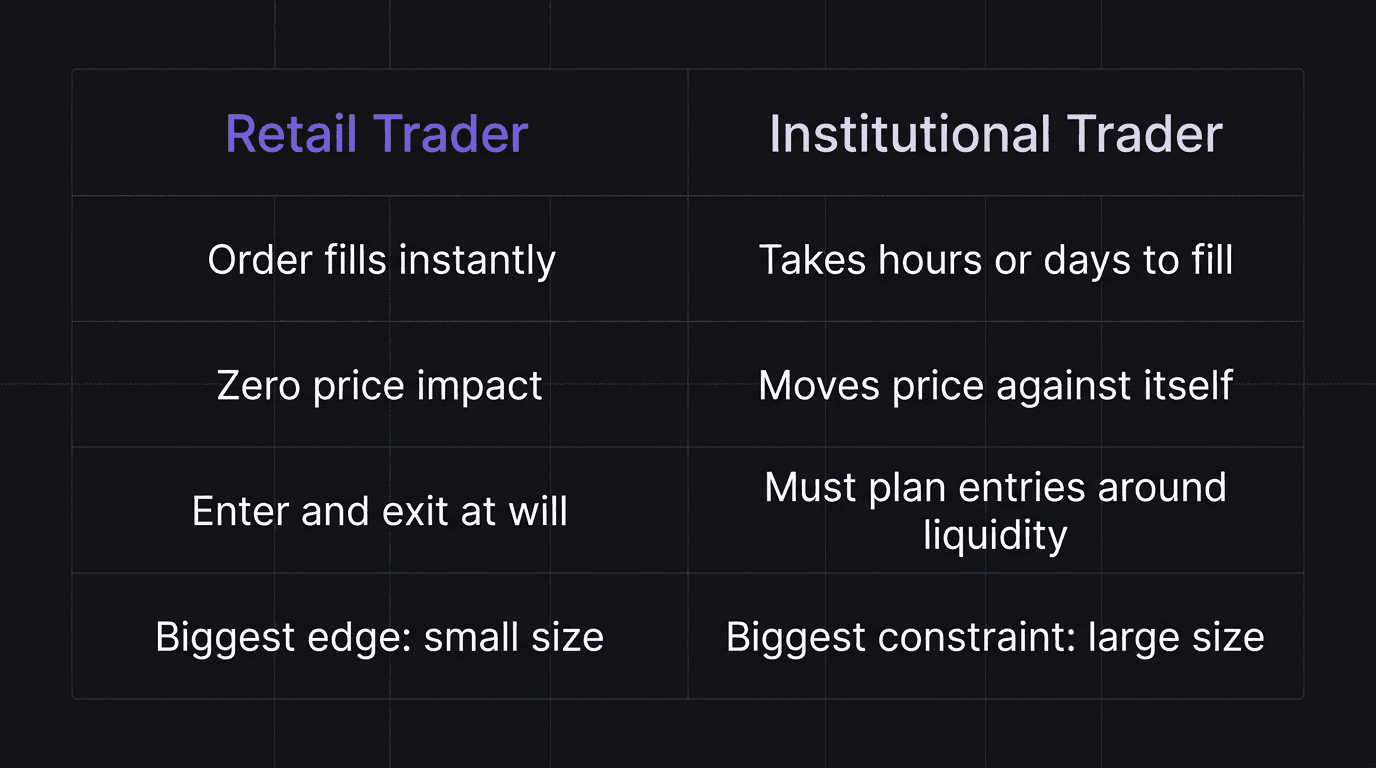

Retail orders fill instantly because your trade size is invisible in a multi-trillion dollar market.

Institutional orders cannot fill at one price without moving the market against themselves.

Institutions accumulate positions gradually and source liquidity from predictable retail stop clusters.

The "manipulation" you feel is institutions filling orders where opposing liquidity is densest.

Aligning with institutional flow means entering after the sweep, not before it.

Why $10K Orders Fill Instantly

You trade a $25,000 account. Your largest position might be 1 standard lot on EUR/USD, which is $100,000 notional. In a market that does $7 trillion daily, your order is background noise. The market does not know you exist.

When you click buy, there are thousands of sell orders already sitting at the ask price. Your 1-lot order absorbs one tiny sliver of that stack and fills instantly. The ask price does not move. The spread does not widen. Nobody on the other side of the market even noticed your trade happened.

This is the privilege of being small. You can enter and exit at the exact price you see on the screen. You can react to setups in real time. You can change your mind and close a position without consequence. These are advantages that institutional traders would pay millions for.

Most retail traders think being "small" is a disadvantage. It is the opposite. Your size is your single biggest edge. You just need to understand why.

The Problem With Million-Dollar Positions

Now imagine you manage a pension fund and you need to buy $200 million worth of EUR/USD. That is 2,000 standard lots. The current ask price shows 50 lots available at 1.0850. If you hit the market with a 2,000-lot order, here is what happens:

The first 50 lots fill at 1.0850. Now the ask moves to 1.0851 where another 40 lots sit. You eat through those. The ask moves to 1.0852. Then 1.0853. Then 1.0855. By the time all 2,000 lots are filled, your average entry price is 1.0870, a full 20 pips worse than where you started.

At $10 per pip per lot on 2,000 lots, that 20-pip slippage costs $400,000. On a single entry.

This is why institutions cannot just click buy. They need strategies to source liquidity without revealing their intention to the market. They break orders into smaller pieces executed over hours or days. They use algorithmic order splitting. And most importantly, they let the market deliver liquidity to them at predictable price levels.

Walkthrough: The institutional entry problem. A hedge fund wants to buy 1,000 lots of GBP/USD. Instead of dumping a market order, they identify a level at 1.2640 where retail stops are clustered below a swing low. They wait. Price drops to 1.2635 as retail stops trigger, flooding the market with sell orders. The fund absorbs those sell orders as the counterparty to their buy. They fill 400 lots at 1.2635 with zero slippage because the sell orders were already there. They repeat this process at the next pool down until the full 1,000 lots are filled.

How Institutions Source Their Liquidity

The most predictable source of opposing orders in the market is retail stop losses. Not because institutions are evil. Because retail traders are predictable.

Swing lows have buy stop losses below them (which trigger as sell orders). Swing highs have sell stop losses above them (which trigger as buy orders). Equal highs and equal lows build even larger pools. These locations are visible to anyone looking at a chart, and institutions look at the same charts you do.

The process works like this:

Institutional trader identifies a zone where they want to accumulate a long position.

They see a large pool of sell stops clustered below a swing low near that zone.

Price drops into the stop cluster. Sell orders flood the market.

The institution absorbs those sell orders as the counterparty, filling their buy position.

Once the pool is drained, there are no more sellers. Price reverses sharply.

This is what a liquidity sweep looks like from the institutional side. It is not manipulation in the criminal sense. It is rational order sourcing at the location where counterparty liquidity is most available.

Aligning With Smart Money Instead of Against It

You have two choices. You can keep placing your stops where every other retail trader places them and donate your orders to institutional positioning. Or you can learn where they source liquidity and position yourself on the same side.

Aligning with smart money does not mean copying their trades (you cannot see their trades). It means understanding their process:

Step 1: Identify the trend direction using market structure. Institutions accumulate in the direction of the higher-timeframe trend, not against it.

Step 2: Map the liquidity pools. Where are the obvious stop clusters below swing lows or above swing highs? Those are the targets.

Step 3: Wait for the sweep. When price moves into the pool and triggers the resting orders, the institutional filling is happening in real time.

Step 4: Enter after the sweep, not before it. Look for a reversal candle, a break of structure on a lower timeframe, or price returning above the swept level as confirmation.

Walkthrough: Aligning instead of donating. EUR/USD shows bullish structure on the 4H chart. Equal lows sit at 1.0800 with a visible supply and demand zone just below at 1.0790. A retail trader buys at 1.0830 with a stop at 1.0795 (below the equal lows). Price sweeps to 1.0788, stops them out, and reverses to 1.0900. An aligned trader waits for the sweep, enters at 1.0795 after a 15m reversal candle, and rides 105 pips. Same setup direction. Different execution. The aligned trader entered where the institutional buying happened instead of being part of the fuel.

The mindset shift is simple: stop trying to predict where price will go. Instead, identify where the market needs to go to source orders, wait for it to get there, and enter after the sourcing is done.

How EdgeFlo Helps You Trade With Structure

Following a multi-step process like institutional alignment requires discipline that breaks down under pressure. The temptation to skip the wait and enter early is strongest when the chart is moving.

EdgeFlo's Edge plan builder lets you write out your mechanical trading plan with clear rules for each step: trend confirmation, liquidity mapping, sweep identification, and entry trigger. The plan stays visible during your session so you cannot "forget" a step when emotions spike.

After each trade, the self-report asks whether you followed the plan or deviated. Over time, you build a dataset of plan adherence versus outcome. The traders who follow the process consistently outperform the ones who skip steps, and the data proves it in your own results, not someone else's.

What is the main difference between institutional and retail traders?

Why do institutions need retail stop losses?

Can retail traders trade like institutions?

Do institutions deliberately manipulate price?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.