Funded Account Management: Keep Your Capital After You Pass

After passing a prop firm challenge, capital preservation becomes priority one. Learn the 5% monthly target, buffer rules, and withdrawal strategy.

Managing a funded account is harder than passing the evaluation. The challenge tested your ability to hit a profit target. The funded phase tests something different: your ability to protect capital, withdraw intelligently, and maintain discipline month after month when the pressure to perform never stops.

Your priorities after funding, in order: preserve capital, hit 5% monthly, maintain your buffer, withdraw only the excess. Break any of these and the account that took you weeks to earn can disappear in days.

TL;DR

Capital preservation is the new priority. The evaluation rewarded aggression. Funding rewards restraint.

Target 5% monthly, not 10%. Five percent is achievable at 30-40% win rate with 1:3 R:R. Ten percent pushes you into reckless territory.

Keep a 2-5% buffer above starting balance at all times. Never withdraw to zero cushion.

Risk 1% standard, 0.5% when below 98% of starting balance (the de-risk trigger).

Journal every trade. Your journal is the early warning system that catches problems before the prop firm does.

The Real Challenge Starts After Funding

Passing a prop firm evaluation feels like crossing a finish line. You hit the target, you stayed within drawdown limits, you proved your strategy works under pressure. Done.

Except you're not done. You just entered a different game.

During the evaluation, you had one job: hit the profit target within the rules. That creates a specific mindset. You're pushing for growth, taking every valid setup, maybe even stretching slightly to meet the deadline.

After funding, that mindset will destroy you. The profit target is still there (most firms require periodic minimums), but the drawdown limit hasn't changed. And now there's real money on the line. Your payouts depend on staying funded, which depends on not hitting maximum drawdown.

Think of the evaluation like qualifying for a race. You drove fast to make the cut. But the race itself rewards consistency and tire management, not raw speed. Same car, completely different approach.

Capital Preservation: Your New Priority

On a funded account, the first rule is simple: don't lose it.

That sounds obvious. But watch how many traders who passed a $100k evaluation blow the funded account within 60 days. They trade the same way they did during the evaluation (aggressive, target-focused, pushing for maximum returns) and run straight into a drawdown wall.

Capital preservation means:

Risk per trade: 1% standard, 0.5% when de-risking. If your account drops below 98% of starting balance, cut size immediately. No debate.

No new strategies on the funded account. Trade the exact system that passed the evaluation. Testing new setups happens on demo or a separate account.

No trading outside your session. If your edge is London session, close the charts during New York. Boredom trades on funded accounts are the most expensive kind.

Pre-market routine every single day. If you haven't done your analysis, you don't trade. Period.

The mental shift is this: your funded account is not an opportunity to get rich. It's a business asset that generates monthly income. You protect business assets. You don't gamble with them.

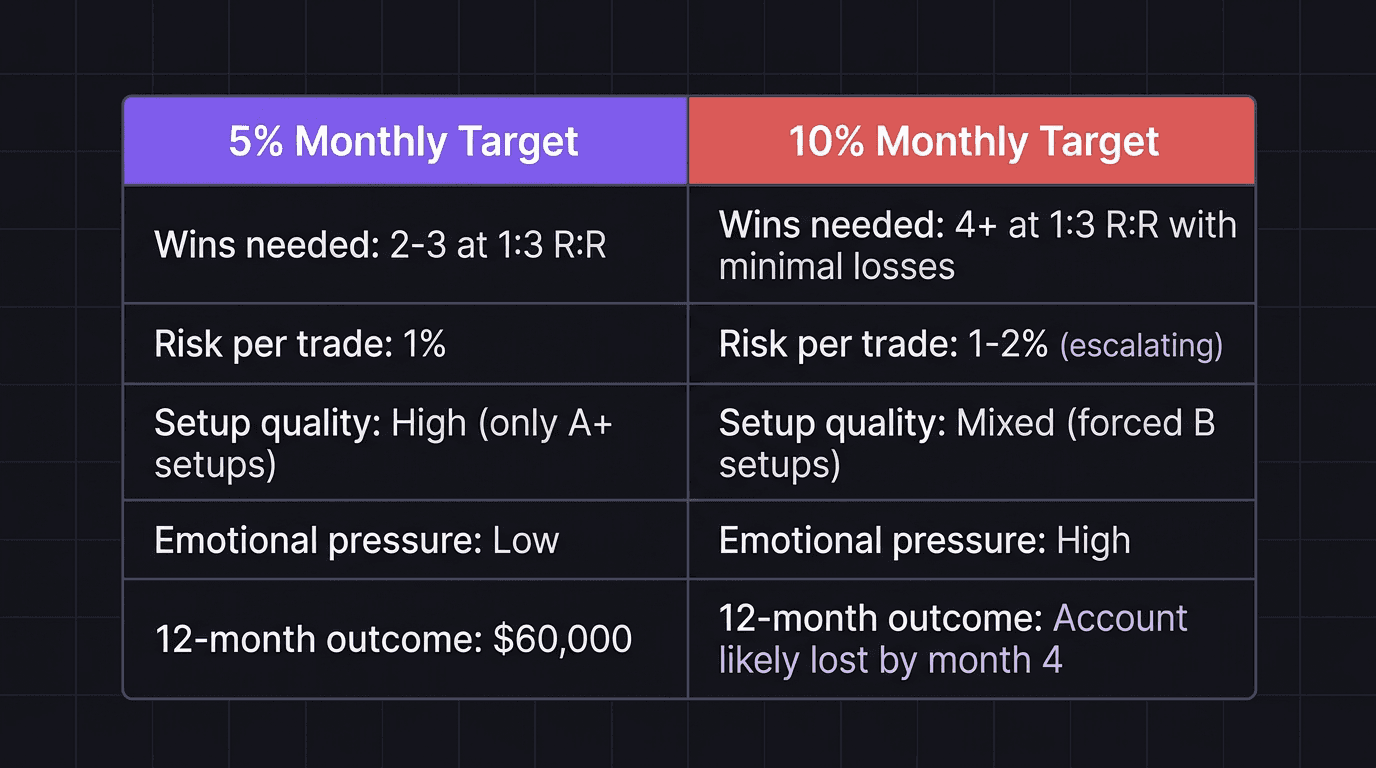

The 5% Monthly Target vs Chasing 10%

Five percent monthly on a $100,000 account is $5,000. That's a meaningful payout. And at 1% risk per trade with a 1:3 minimum R:R, you need roughly two winning trades per month to get there (each winner returns 3%).

Now look at 10%. That's $10,000 per month. At 1% risk with 1:3 R:R, you need about 3-4 winners with almost no losers. Possible in a great month. Impossible to sustain.

What happens when you target 10%? You're at 6% profit with one week left. You start taking setups you'd normally skip. You trade during off-hours because you "might catch a move." You widen your risk to 2% because "I just need one more winner." Sound familiar?

That's how funded accounts get blown. Not from bad strategy. From good strategy corrupted by unrealistic targets.

Target | Risk Behavior | Sustainability |

|---|---|---|

5%/month | Normal setups, normal risk, normal sessions | High |

10%/month | Forced setups, expanded risk, extra sessions | Low |

15%+/month | Gambling disguised as trading | Near zero |

Five percent is the target that lets you trade normally. You don't need to force anything. Your regular strategy works without modification. And when you have a bad week, you're not panicking because 5% leaves room for recovery within the same month.

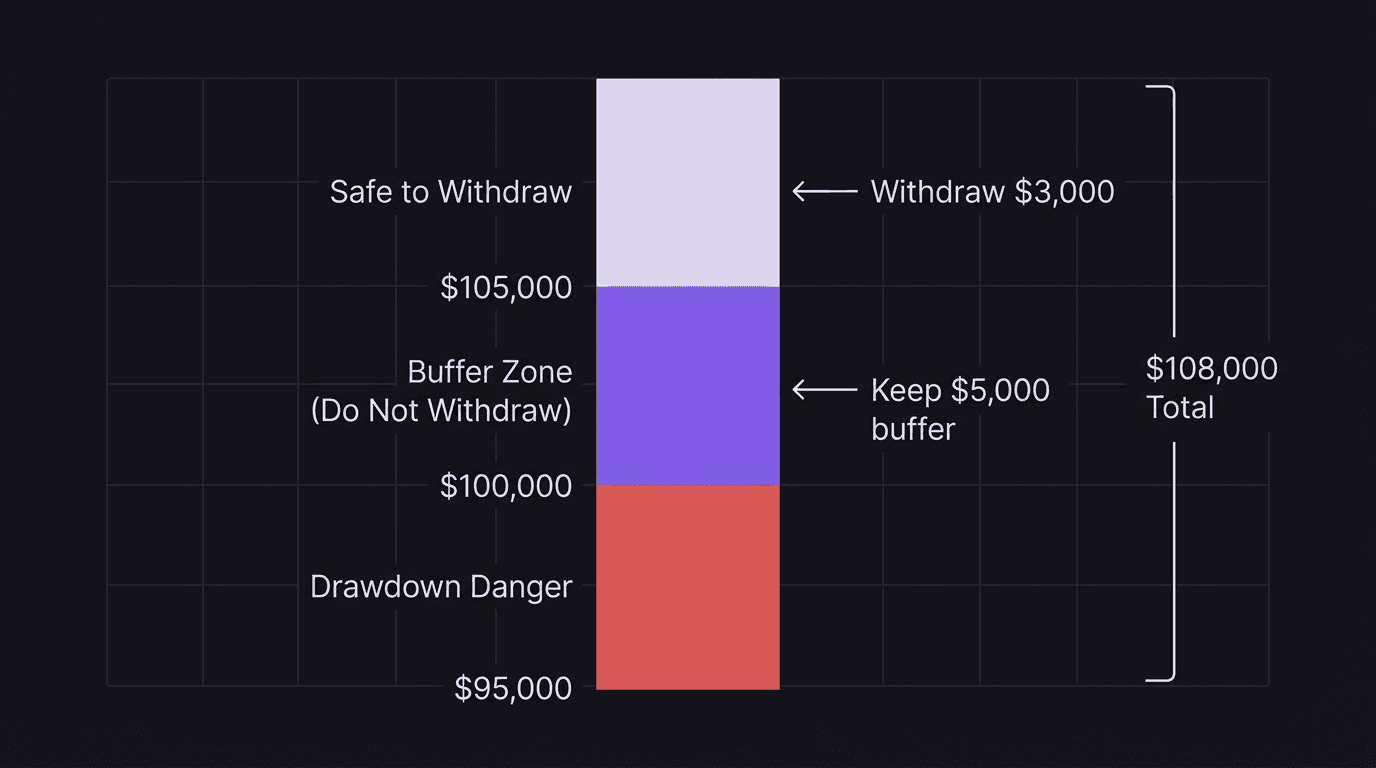

Withdrawal Strategy: Don't Empty Your Buffer

Payout day is when most funded traders make their biggest mistake. The account is at $108,000. You withdraw $8,000. Balance goes back to exactly $100,000.

Then Monday happens. Two losing trades at 1% risk each. Balance: $98,000. You're now 2% in drawdown with zero cushion. Three more losses and the firm is sending you an email about drawdown limits.

The buffer rule: always keep 2-5% above your starting balance.

Withdraw: $3,000

Buffer remaining: $5,000

New balance: $105,000

If those same two Monday losses hit, you're at $103,000. Still in profit. Still comfortable. Still trading without fear.

Walkthrough: Two Traders, Same Month, Different Withdrawals

> Trader A has a $100k funded account. End of month 2, balance is $109,000. She withdraws $4,000 and keeps a $5,000 buffer. Balance: $105,000. > > Week 1 of month 3: three losing trades on EUR/USD at 1% risk each (-$3,150 total). Balance: $101,850. She's still above starting capital. Her emotional state: calm. She sticks to her trading plan and takes two winners later that week at 1:3 R:R (+$6,300). Month 3 ends at $108,150. > > Trader B has the same account, same balance at $109,000. He withdraws all $9,000. Balance: $100,000. > > Same three losing trades at 1% risk, but his balance is $100,000 so each loss is $1,000. Total: -$3,000. Balance: $97,000. He's $3,000 below starting capital. Drawdown limit is $95,000. He's $2,000 away from losing the account. > > His emotional state: panicked. He cuts his risk to 0.25% (too low to recover meaningfully) or does the opposite and increases to 3% trying to claw back the losses (revenge trading territory). Either way, the account is in danger.

Same strategy. Same month. Different outcomes. The only difference was how much each trader kept in the account.

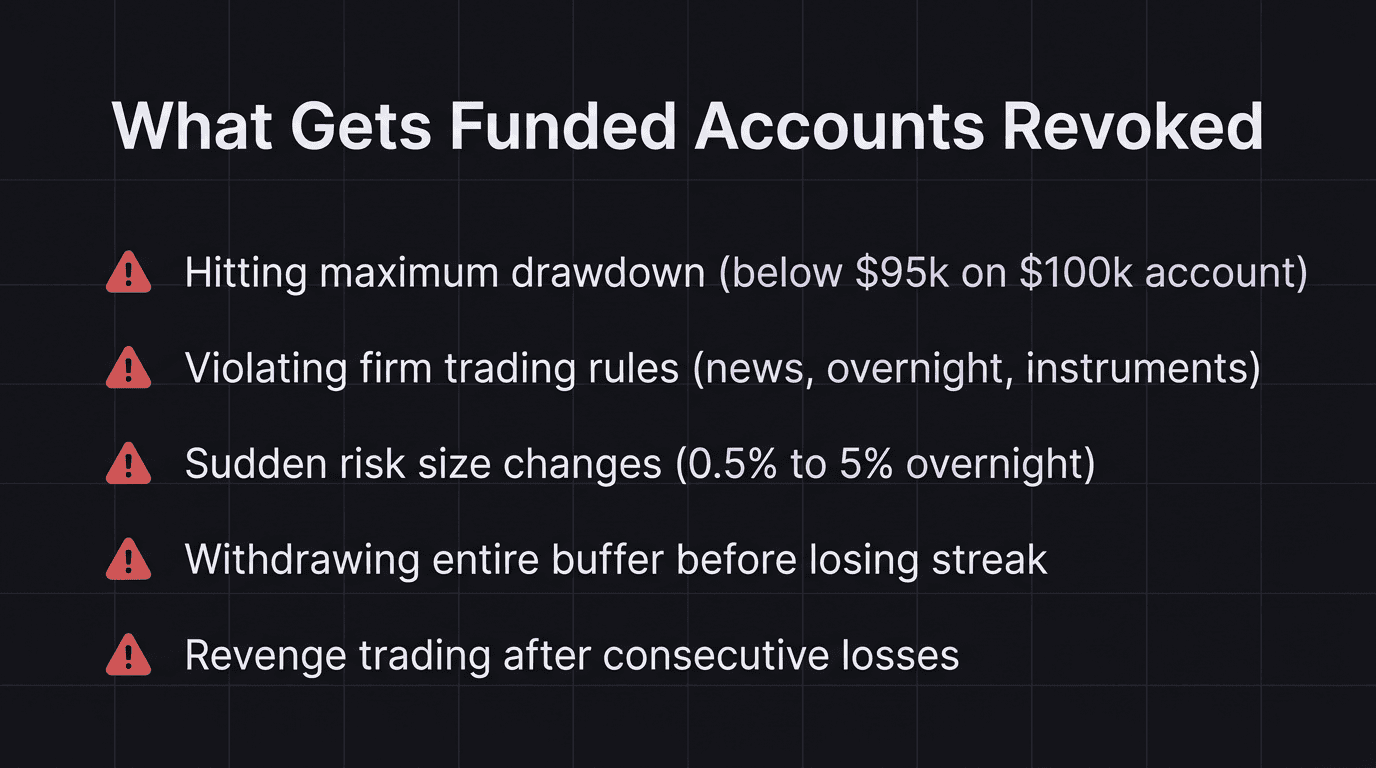

What Gets Funded Accounts Revoked

Prop firms revoke accounts for specific, predictable reasons. Knowing what kills accounts is just as valuable as knowing what sustains them.

1. Hitting maximum drawdown. This is the most common killer. Most firms set a 5-10% maximum drawdown from peak balance. On a $100k account with a 5% limit, dropping below $95k means immediate termination. No second chances.

2. Violating trading rules. Some firms restrict news trading, overnight holds, or specific instruments. Breaking these rules, even while profitable, gets accounts revoked. Read the fine print before you trade, not after.

3. Inconsistency patterns. Some firms flag accounts that show wildly different position sizes or sudden strategy changes. If you've been risking 0.5% for three months and suddenly jump to 5%, that triggers review.

4. Withdrawing into vulnerability. Not a direct rule violation, but the behavior that leads to #1. Empty your buffer, hit a normal losing streak, and you're done.

5. Revenge trading after losses. The revenge trading cycle is responsible for more blown funded accounts than any market event. Two losses become four because the trader couldn't walk away. The firm doesn't care why you lost 7% in a day. They just see the drawdown.

Every one of these is preventable. That's the frustrating part. Funded accounts don't get revoked by bad luck. They get revoked by bad decisions that the trader knew were bad while making them.

What separates traders who keep their accounts for years from those who lose them in months? Journaling habits. Traders who review their data weekly catch problems at -2% drawdown. Traders who don't catch problems at -5%, when it's too late.

How EdgeFlo Protects Funded Accounts

The difference between knowing the rules and following them is execution. On a Tuesday after three losses, knowing you should de-risk to 0.5% doesn't guarantee you'll actually do it. Especially when the next setup looks perfect and you want to recover fast.

EdgeFlo's guardrails enforce max daily loss and risk per trade limits. If you set your max daily loss to 2% and you've already lost 1.8%, EdgeFlo flags the next trade. The Trade button disables with an override option. You can still take the trade (the override is always available), but you have to consciously choose to break your own rule. That pause is where most trading mistakes get caught.

The dashboard includes a Discipline Summary showing your current guardrail status. At a glance: how much drawdown room you have left today, how close you are to your risk per trade limit, and whether your current position sizing matches your rules. For funded traders, this visibility is the difference between catching a problem at -2% and discovering it at -5%. By then, the math to recover is brutal and the emotional pressure makes disciplined trading nearly impossible.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

How do I manage a funded trading account?

What is a good monthly target for a funded account?

Why do funded traders lose their accounts?

How much should I withdraw from a funded account?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.