Total Loss Risk: The Number That Predicts Account Failure

Total loss risk tells you the probability of blowing your account. Learn how to calculate it, track it on your dashboard, and keep it near zero.

Total loss risk is the probability that your trading system will drain your account to zero over a set number of trades. It is the single most important number in your risk management dashboard because it answers one question every other metric avoids: what is the chance that this system kills my account?

At 2% risk per trade with a 30% win rate and 1:5 risk-to-reward, your total loss risk is 23% over 30 trades. At 0.5% risk with the same strategy, it is 0.1%. Most traders track win rate, profit factor, and maybe expectancy. Almost none track total loss risk. That is why they are surprised when a normal losing streak turns into an account blow-up.

TL;DR

Total loss risk measures the probability of complete account wipeout over a set number of trades.

It depends on three inputs: risk per trade, win rate, and average R:R ratio.

At 2% risk per trade (30% WR, 1:5 R:R, 30 trades), total loss risk is 23%.

At 0.5% risk with the same parameters, it drops to 0.1%.

Tracking this metric on your trading dashboard catches sizing problems before they become account-ending problems.

Why Total Loss Risk Is Different from Drawdown

Most traders think about risk in terms of drawdown: "How much can I lose before I recover?" That is useful but incomplete. Drawdown tells you about depth. Total loss risk tells you about probability of death.

A 20% drawdown is painful but survivable. You need about a 25% gain to recover, and a sound strategy will generate that over time. Total loss risk asks a different question: over the next 30 (or 100) trades, what is the chance that the sequence of wins and losses is bad enough to take the entire account?

The distinction matters because a strategy with attractive average returns can still carry unacceptable ruin probability. A 53% average return sounds excellent until you learn that the same system has a 23% chance of zero balance. Would you fly on an airline with a 23% crash rate? Same logic applies to your capital.

How Total Loss Risk Is Calculated

Total loss risk comes from Monte Carlo simulation. Here is the process:

Define your parameters: risk per trade, win rate, reward ratio, and trade count.

Run 100+ random simulations using those parameters. Each simulation generates a random sequence of wins and losses based on the win rate probability.

Count how many simulations end at zero (or below a defined threshold).

That percentage is your total loss risk.

The reason you need simulations (not just a formula) is that trade sequence matters. A strategy might be profitable on average, but a specific sequence of early losses can create a hole so deep that subsequent wins cannot fill it. Monte Carlo captures this by testing thousands of possible sequences.

Walkthrough: Building a Total Loss Risk Estimate

You trade EUR/USD. Your backtest over 200 historical trades shows:

Win rate: 32%

Average winner: 4.8R

Average loser: 1R

Risk per trade: 1% of account

Your trading expectancy per trade:

Expectancy = (0.32 times 4.8R) minus (0.68 times 1R)

Expectancy = 1.536R minus 0.68R

Expectancy = +0.856R per trade

Positive expectancy. Good. But expectancy alone does not tell you the ruin probability. You run 100 Monte Carlo simulations of 50 trades each at 1% risk.

Results: 4 out of 100 simulations hit zero. Total loss risk: 4%.

That means roughly 1 in 25 paths through 50 trades ends in total wipeout, even with a positive-expectancy system. If you traded this for five years (several 50-trade cycles), there is a meaningful chance one of those cycles destroys the account.

Now you reduce risk to 0.5% per trade and rerun. Results: 0 out of 100 simulations hit zero. Total loss risk: below 1%.

Same strategy. Same edge. The only change was halving the risk per trade. The total loss risk became negligible.

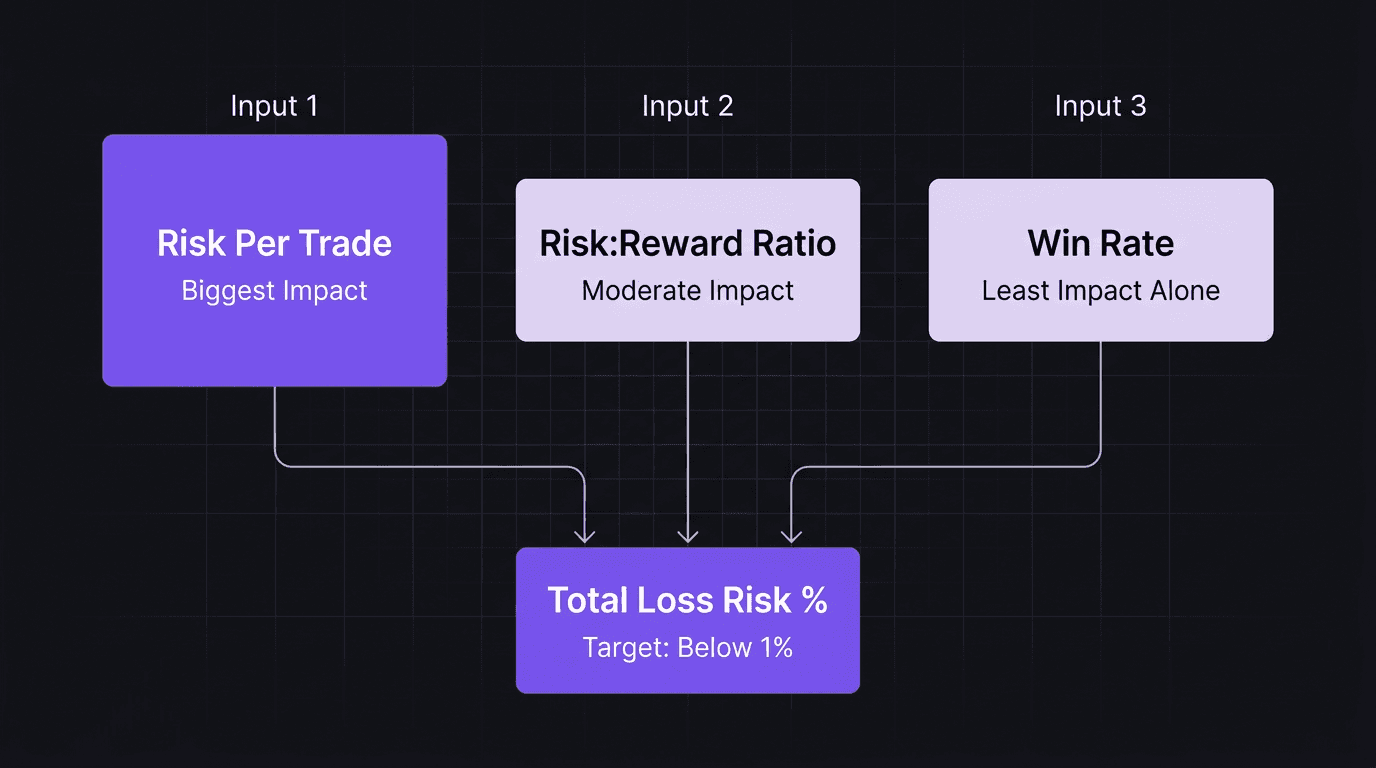

The Three Inputs That Control Total Loss Risk

1. Risk Per Trade

This is the biggest lever. Moving from 2% to 0.5% per trade can shift total loss risk from 23% to 0.1%. No other adjustment has this much impact.

Risk per trade determines how many trades you can lose before the account hits zero. At 1% risk, you have 100 bullets. At 0.5%, you have 200. The more bullets you carry, the more likely your positive-expectancy edge has time to express itself across a large sample.

If you are unsure where to set yours, read the risk per trade decision framework.

2. Risk-to-Reward Ratio

A higher R:R means each winning trade recovers more lost ground. At 1:5, each win covers five losses. At 1:2, each win only covers two. With a 30% win rate, the difference between these two ratios is the difference between a profitable system and a losing one.

3. Win Rate

Win rate matters, but less than most traders assume. A 30% win rate with 1:5 R:R and 0.5% risk gives you 0.1% total loss risk. A 50% win rate with 1:2 R:R and 2% risk might give you 15% or more.

The combination matters more than any single input. That is why total loss risk is calculated through simulation, not estimated by gut feel.

What the Numbers Look Like at Different Risk Levels

Here is the data across three risk levels, all using the same strategy: 30% win rate, 1:5 R:R, 30-trade window, $100,000 account.

Total loss risk: 23%

Average return: +53%

Best case: +200%

Worst case: negative 11.7%

Total loss risk: 3%

Average return: +26%

Best case: +100%

Worst case: negative 10%

Total loss risk: 0.1%

Average return: +14%

Best case: +40%

Worst case: negative 3.5%

The pattern is clear: as risk per trade decreases, total loss risk falls dramatically while average returns decrease more modestly. The ratio of safety to performance shifts heavily in your favor at lower risk levels.

Walkthrough: Using Total Loss Risk to Evaluate Your System

You have been trading live for three months. Your journal shows:

45 trades taken

14 wins, 31 losses

Win rate: 31.1%

Average winner: 4.2R

Average loser: 1.0R

Current risk per trade: 1.5%

Step 1: Calculate expectancy. Expectancy = (0.311 times 4.2R) minus (0.689 times 1.0R) = 1.306R minus 0.689R = +0.617R per trade.

Step 2: Estimate total loss risk. With 1.5% risk per trade and a 31% win rate at 4.2R, your total loss risk over the next 50 trades is likely between 5% and 10%.

Step 3: Evaluate. Your expectancy is positive, which is good. But a 5% to 10% total loss risk means roughly 1 in 10 to 1 in 20 50-trade stretches could wipe you out. Over a year of trading (200+ trades, or four 50-trade cycles), that compounds into uncomfortable territory.

Step 4: Adjust. Drop risk per trade from 1.5% to 0.75%. Your average returns will decrease, but your total loss risk drops below 1%. You trade the same system, the same setups, the same entries. The only change is position sizing.

Putting Total Loss Risk on Your Dashboard

Total loss risk is not a metric you check daily. It is a strategic number you evaluate monthly or after any significant change to your system.

Track these on your trading dashboard:

Current risk per trade setting (your rule, not your average)

Actual risk per trade (what you actually risked, from journal data)

Rolling win rate (last 50 to 100 trades)

Average R per winner and loser

Estimated total loss risk (recalculate monthly or after rule changes)

If your actual risk per trade is consistently higher than your rule (you keep oversizing), your total loss risk is higher than you think. The dashboard catches this drift before it costs you.

The most actionable use: when your actual risk per trade creeps above your rule, that is the moment to stop trading and fix the sizing problem. Not after a drawdown. Not after a blow-up. Now, while the deviation is small.

How EdgeFlo Surfaces Total Loss Risk

EdgeFlo's trading dashboard tracks your risk per trade on every entry, not just what you planned but what you actually risked. The discipline summary shows whether your real positions match your stated rules.

The weekly AI report compares your current risk metrics against your historical baseline. If your average risk per trade is creeping up (common after a winning streak triggers complacency), the report flags it. You can catch the drift early, before it shifts your total loss risk from safe to dangerous.

EdgeFlo's performance analytics also calculate your rolling expectancy and R statistics. Combined with your risk-per-trade data, you have the inputs needed to estimate total loss risk without running separate simulations. The pattern recognition works in your favor: consistent risk per trade plus positive expectancy equals sustainable trading.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

What is total loss risk in trading?

How do you calculate total loss risk?

What is a safe total loss risk percentage?

Does win rate affect total loss risk?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.