Prop Firm Scaling: From $100k to $400k Without Increasing Risk

Scale your prop firm capital from $100k to $400k by reinvesting payouts into new funded accounts. Step-by-step plan with buffer strategy and risk math.

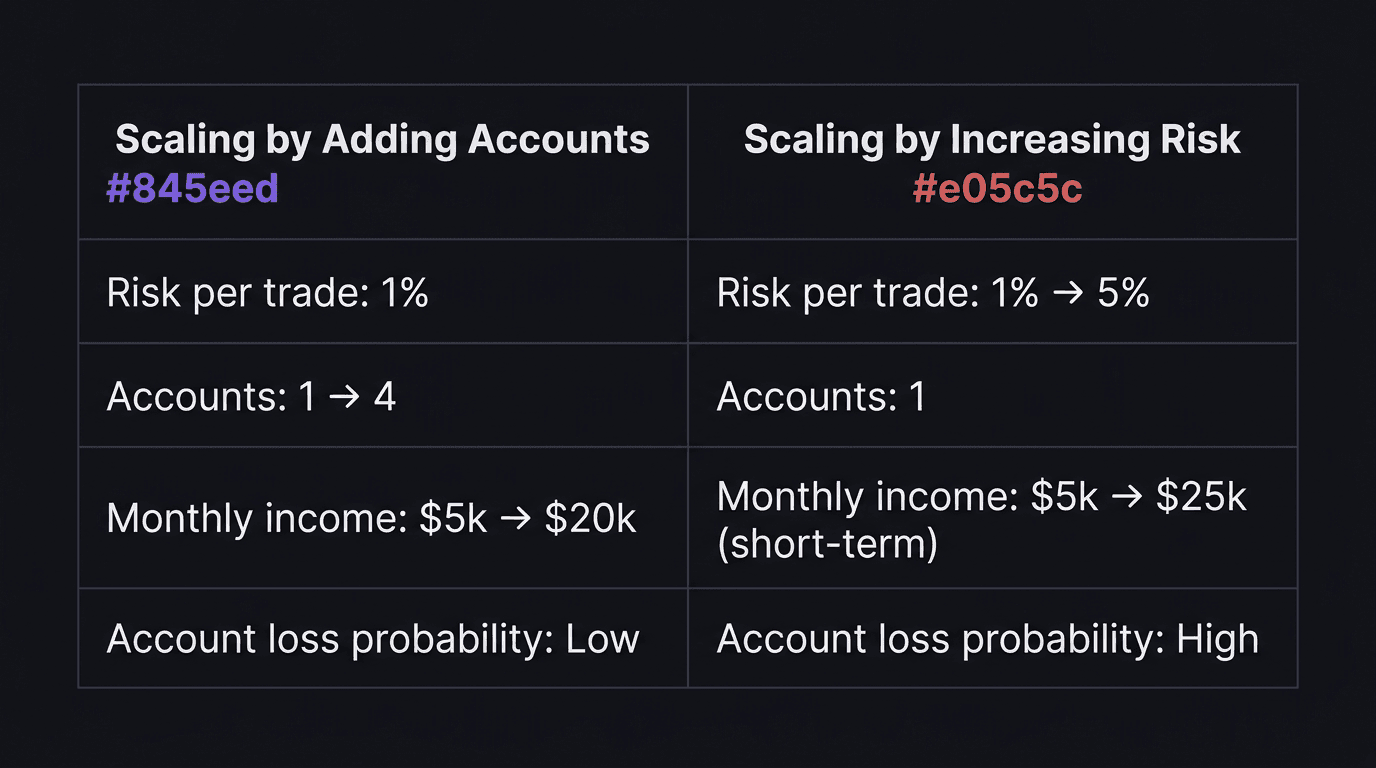

Scaling a prop firm account means adding more funded accounts, not taking bigger risks on the one you have. Start with a single $100k account, hit 5% monthly for 2-3 months, then reinvest payouts into a second $100k challenge. Two accounts at 5% each gives you $10,000 per month. Four accounts, same risk per trade, same strategy: $20,000 per month.

The math works because you're multiplying capital, not multiplying risk. Your risk per trade stays at 1%. Your strategy stays identical. The only thing that changes is how many accounts run simultaneously.

TL;DR

Scale capital by adding funded accounts, not by increasing lot sizes or risk percentage.

5% monthly target per account is achievable with a 30-40% win rate and 1:3 minimum R:R.

Reinvest payouts into new challenges after 2-3 months of proven consistency.

Keep a 2-5% buffer in each account to survive normal drawdown swings.

Four $100k accounts at 5% = $20k/month, or $240k/year, all at 1% risk per trade.

Why Scaling Capital Beats Increasing Risk

Most traders try to grow income by taking bigger positions. They bump risk from 1% to 3%, then 5%. It works for a week. Then one losing streak puts them in the drawdown zone, and the account is gone.

Scaling capital is the opposite approach. You keep risk per trade at exactly 1% (or even 0.5% during drawdowns). You keep the same pairs, same setups, same session. But you run the strategy across two, three, or four funded accounts instead of one.

Think of it like opening a second location of a profitable restaurant. You don't make the portions bigger at the first location. You replicate the system that already works.

The math makes this clear:

Accounts | Total Capital | Monthly at 5% | Annual |

|---|---|---|---|

1 | $100,000 | $5,000 | $60,000 |

2 | $200,000 | $10,000 | $120,000 |

3 | $300,000 | $15,000 | $180,000 |

4 | $400,000 | $20,000 | $240,000 |

Same strategy. Same discipline. Same 1% risk. The income quadruples because the capital quadruples.

The 5% Monthly Target (And Why 10% Is Dangerous)

Five percent monthly sounds modest. It is. That's the point.

At 1% risk per trade with a 1:3 reward-to-risk ratio, one winning trade returns 3%. Two winners in a month gets you to 6%, even if you lose five other trades in between. A 30-40% win rate is enough.

Chasing 10% monthly is where accounts die. To hit 10% on a $100k account, you need $10,000 in profit. At 1% risk, that's roughly 3-4 winning trades with zero losers. Possible? Sure. Sustainable month after month? Almost never.

The real danger: when you're at 7% with a week left and you start forcing trades to hit 10%. You widen your risk. You take setups you'd normally skip. You trade outside your session. Sound familiar?

Five percent keeps you in a rhythm where normal trading mistakes don't spiral. You can have a rough week and still finish the month positive. At 10%, every losing day feels like a crisis.

Walkthrough: The 5% Month in Practice

> You're trading GBP/USD on a $100,000 funded account during London session. Risk per trade: 1% ($1,000). Your minimum R:R is 1:3. > > Week 1: Two setups. One winner at 1:3 (+$3,000), one loser (-$1,000). Net: +$2,000. > Week 2: Three setups. One winner at 1:3 (+$3,000), two losers (-$2,000). Net: +$1,000. > Week 3: Two setups. Both losers (-$2,000). Net: -$2,000. > Week 4: Two setups. One winner at 1:5 (+$5,000), one loser (-$1,000). Net: +$4,000. > > Monthly total: +$5,000 (5%). Win rate: 33% (3 wins out of 9 trades). One great trade in week 4 saved the month. That's how 1:3+ R:R works. You don't need to win often. You need your winners to be big.

Reinvesting Payouts Into New Accounts

Here's where the scaling actually happens. After 2-3 months of consistent 5% returns, you've proven the strategy works on live capital. Time to add a second account.

Most prop firms let you withdraw monthly. If you've been making $5,000 per month and living expenses are covered, that payout funds your next $100k challenge. Challenge fees typically run $500-$1,000 for a $100k account.

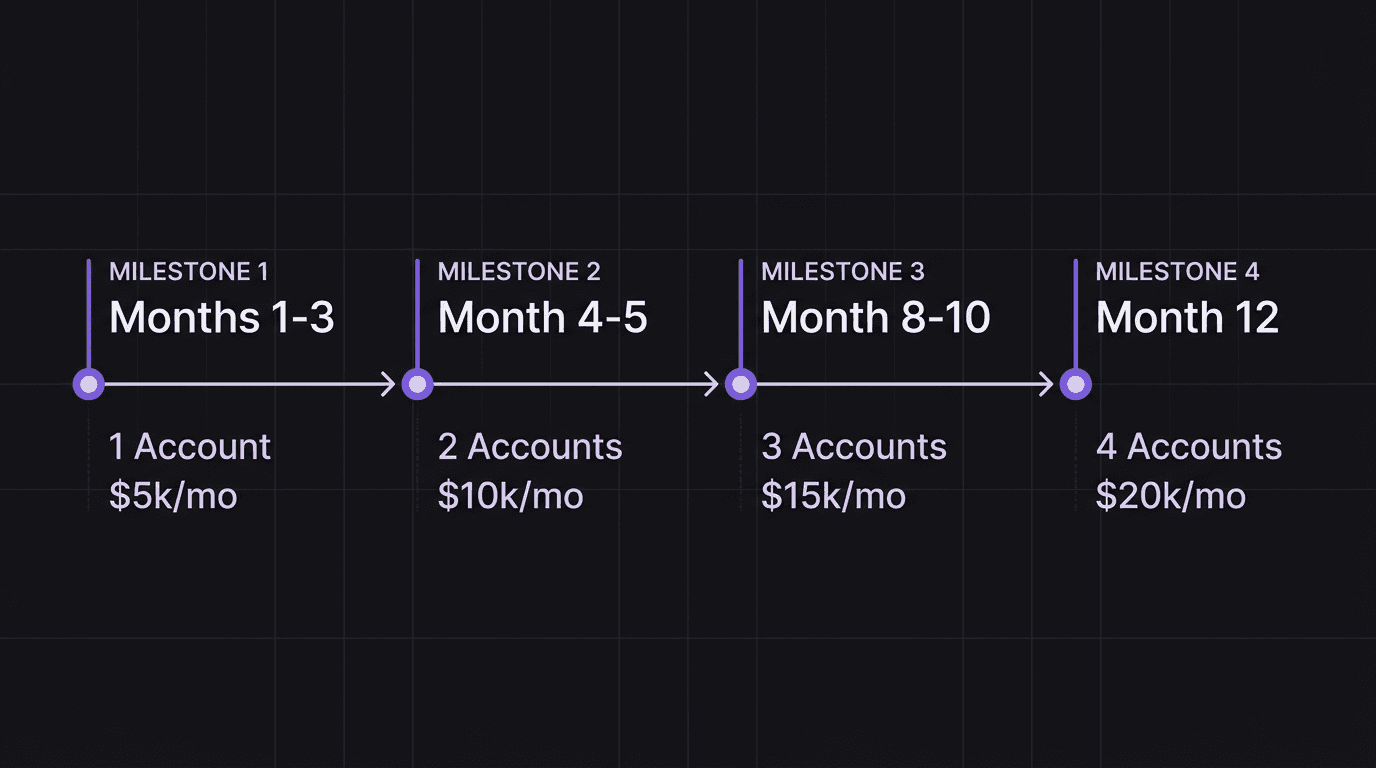

The timeline looks like this:

Months 1-3: Trade one $100k account. Prove consistency. Build a track record.

Month 4: Use accumulated payouts to buy a second $100k challenge. Pass it using the same strategy.

Months 5-7: Trade both accounts simultaneously. Income doubles to $10k/month.

Month 8-10: Add a third account. Income: $15k/month.

Month 12: Four accounts running. $20k/month at 5% each. Annual run rate: $240k.

The key: do not rush. If month 2 was a struggle and you barely hit 3%, you're not ready for a second account. Consistency first. Scaling second.

Managing Multiple Funded Accounts

Running four accounts sounds like four times the work. It isn't, if you do it right.

Every account trades the same strategy, same pairs, same session. You're not running four different approaches. You're copying one approach across four execution environments.

The practical workflow:

Same pre-market routine for all accounts. One analysis session covers every account. You're looking at the same charts.

Sequential execution. Take the setup on Account 1, then immediately replicate on Account 2, 3, and 4. Same entry, same stop, same target.

Separate journal entries per account. Even though the trade is identical, each account has its own P&L, its own buffer level, and its own drawdown status.

Where traders fail with multiple accounts: they start improvising. They take a "bonus setup" on Account 3 that they skipped on Account 1. They move the stop on one account but not others. Now they're running different strategies without realizing it.

One strategy. Multiple copies. That's the rule.

The Buffer Strategy: Keep 2-5% in Reserve

This is the rule that keeps funded accounts alive during losing streaks. Never withdraw everything above your starting balance.

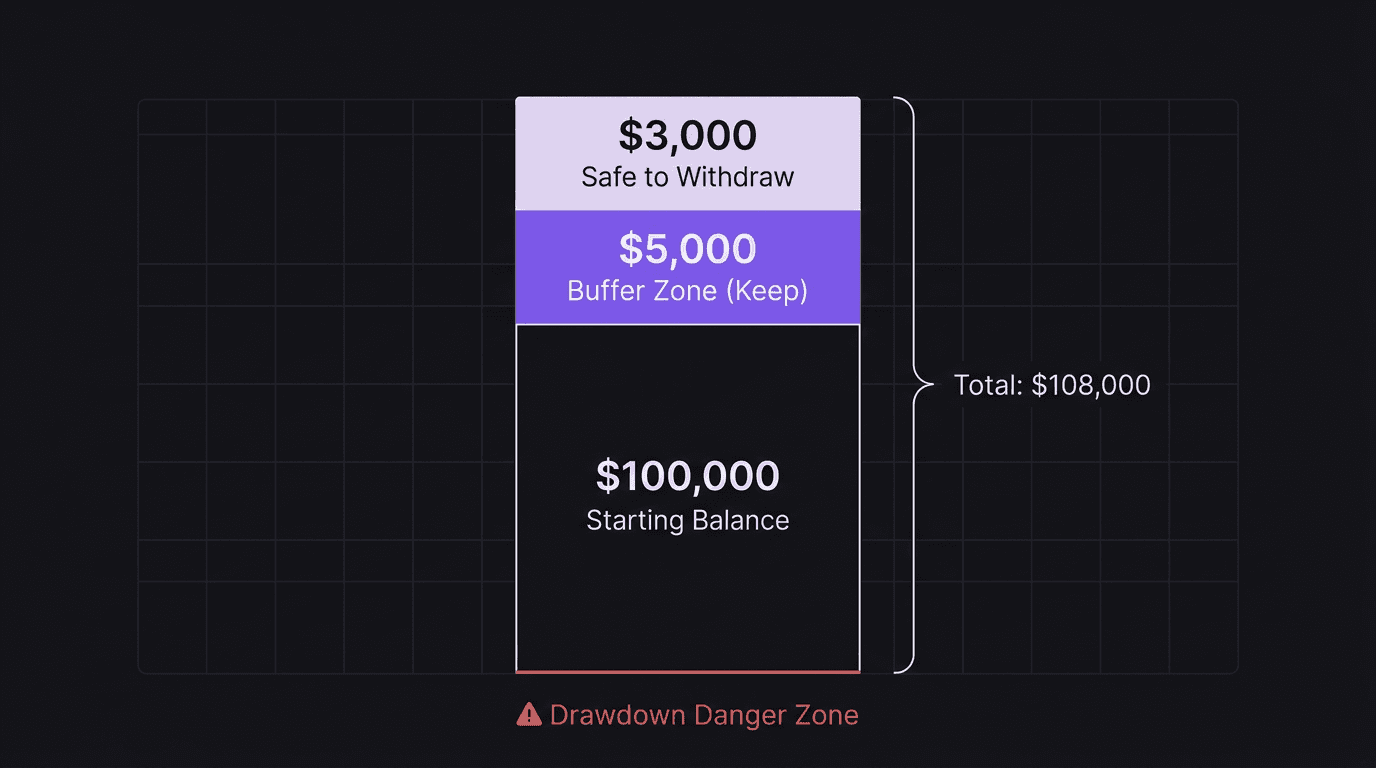

Here's the math. Your $100k account grows to $108,000 over two months. The instinct is to withdraw $8,000. Don't.

Withdraw $3,000. Leave $5,000 as a buffer. Your account sits at $105,000.

Why? Because losing streaks happen. If you withdraw to exactly $100,000 and then lose your first two trades at 1% risk, you're at $98,000. That's a $2,000 drawdown on an account with zero cushion. Some firms flag accounts at 4-5% drawdown. You're already halfway there after two trades.

With a $5,000 buffer, those same two losses put you at $103,000. Still profitable. Still comfortable. Still trading with full confidence.

The buffer rules:

Minimum buffer: 2% of starting capital ($2,000 on a $100k account)

Recommended buffer: 5% ($5,000 on a $100k account)

When to withdraw: only the amount above your buffer threshold

When up 8% over two months: withdraw 3%, leave 5% buffer, balance stays at $105k

What Happens Without a Buffer

> You're trading EUR/USD on a $100k funded account. End of month 2, balance is $108,000. You withdraw the full $8,000. > > Week 1 of month 3: three losing trades at 1% risk each. Balance drops to $97,000. The prop firm's maximum drawdown limit is $94,000. You're now just $3,000 away from losing the account. > > Your risk behavior changes. You start hesitating on valid setups. You cut winners early because you can't afford another loss. You skip your London session trade because the spread feels too wide. > > If you'd kept a 5% buffer, those same three losses would put you at $105,000 minus $3,000 = $102,000. Still in profit. Still trading normally. The buffer bought you space to lose without panicking.

When your buffer drops below 2%, shift to de-risk mode. Cut risk per trade to 0.5%. At 0.5% risk with a 1:3 R:R, one winner returns 1.5%, which recovers roughly a 2.5% drawdown. You're always one trade away from recovery.

How EdgeFlo Supports Multi-Account Discipline

Running multiple funded accounts means tracking multiple balances, multiple drawdown levels, and multiple buffer thresholds simultaneously. That's where things slip.

EdgeFlo connects to MT4, MT5, and cTrader, syncing balances, positions, and orders in real time across all your accounts. You see every account's status on one dashboard instead of switching between four broker terminals.

The practical benefit for scaling: when Account 2 drops below its buffer threshold, you can see it immediately and shift to 0.5% risk on that account while keeping 1% risk on the others. Without centralized tracking, these kinds of per-account adjustments get missed. And missed adjustments are how funded accounts get revoked.

Pair this with journal entries per account. When you review your month, you want to see which accounts performed differently and why. Maybe Account 3 had slippage issues during NFP because you were slow on execution. That's the kind of detail that helps you decide whether to add a fourth account or tighten your process on the existing three. Your backtesting results become the baseline you measure live performance against.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

How do I scale my prop firm account?

How much should I withdraw from a funded account?

Is 5% monthly realistic for funded traders?

How many funded accounts should I have?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.