Funded Challenge Budget: Only Risk Disposable Income

Never fund a challenge with money you need for bills. Learn how to set a funded challenge budget using disposable income so pressure does not destroy your trading.

Why Your Challenge Budget Determines Your Trading Quality

The biggest funded challenge mistake has nothing to do with chart analysis. It happens before you ever place a trade. It happens the moment you pay for a challenge with money you cannot afford to lose.

When the fee is your rent money, your grocery money, or the last cash in your account, every trade carries a weight it was never supposed to carry. You stop trading your plan and start trading your anxiety.

TL;DR

Only fund a challenge with disposable income, the money left after all bills and essentials are paid.

If losing the fee would cause financial stress, the account size is too big for your budget.

Challenge fees are a sunk cost the moment you pay them. Treat them as money already gone.

Budget for multiple attempts, not just one. Most traders do not pass the first time.

The right budget removes pressure so you can actually follow your plan.

Disposable Income: The Only Money That Qualifies

Disposable income is what remains after you have paid rent, utilities, food, transportation, savings, and every other non-negotiable expense. It is the money you could light on fire and your life would not change.

That is the only pool your challenge fee should come from.

A $100,000 account challenge costs roughly $600. A $50,000 account runs about $345. A $10,000 account can be under $100 at some firms.

If your disposable income after all expenses is $1,000, a $600 fee is possible but aggressive. You are committing 60% of your discretionary money to a single attempt with roughly a 70% to 80% failure rate.

If your disposable income is $200, the $10,000 account at $89 is your lane. There is no shame in that. The account size does not determine your skill level. It determines your financial readiness.

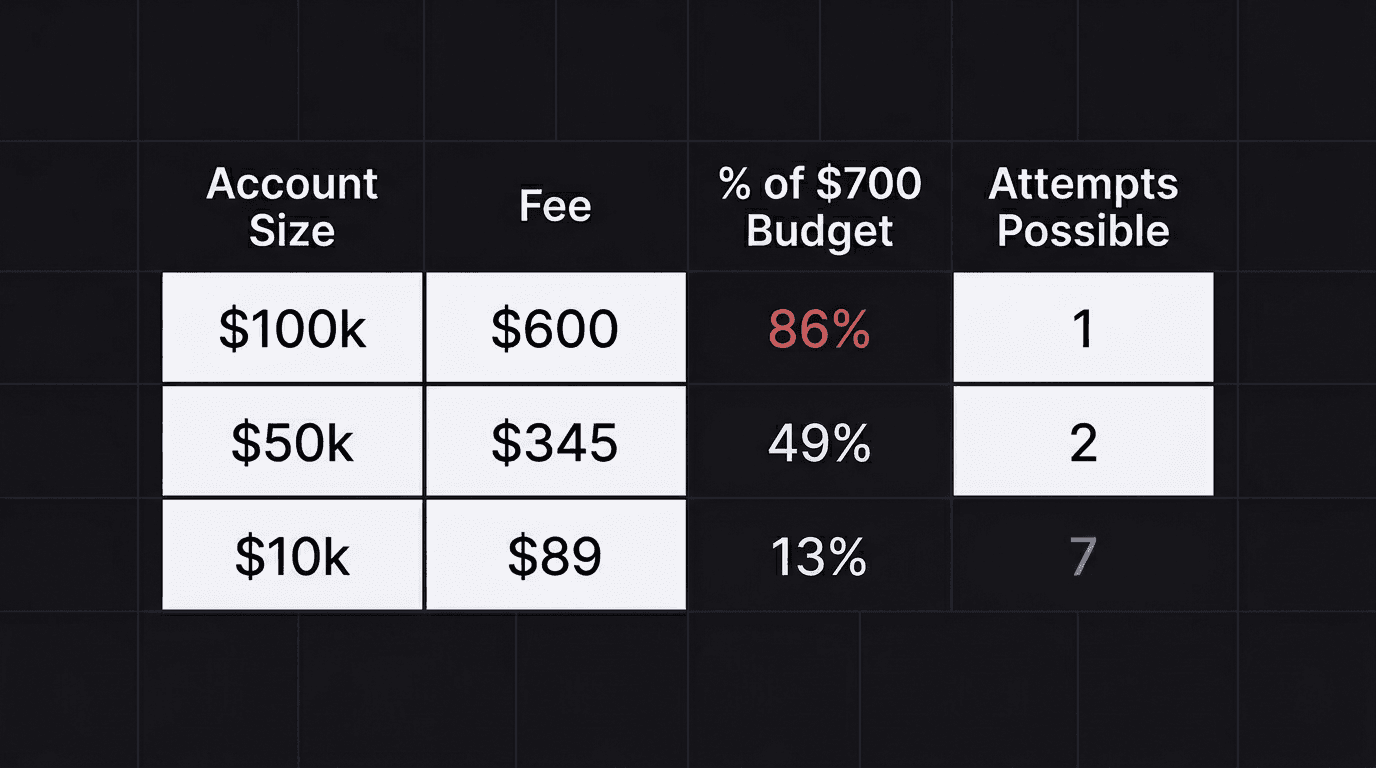

Walkthrough: Matching Budget to Account Size

Imagine you earn $3,500 per month. Your fixed expenses (rent, food, transport, insurance, subscriptions, savings) total $2,800. That leaves $700 in disposable income.

Option A: $100k challenge at $600. That is 86% of your disposable income on a single attempt. If you fail, you have $100 left for the month. The next attempt waits until next month at minimum.

Option B: $50k challenge at $345. That is 49% of your disposable income. You could attempt twice in one month if the first attempt fails early.

Option C: $10k challenge at $89. That is 13% of your disposable income. You could afford up to 7 attempts from a single month's discretionary budget.

Option C gives you the most attempts and the least pressure per attempt. A smaller account with calm execution beats a large account with shaking hands.

The Fee Is Gone the Moment You Pay It

Here is the mental shift that changes everything: the second you pay the challenge fee, that money no longer exists. It is not sitting in an escrow waiting for you. It belongs to the firm.

Yes, if you pass both phases, the fee gets refunded. But you cannot trade with the expectation of getting it back. That expectation is poison.

When you expect the refund, every losing trade feels like it is stealing from you personally. Your stop loss hits and your brain screams "that is $50 of my fee I will never see again." That thought has zero logical connection to trading, but it takes over anyway.

The traders who handle challenges best are the ones who wrote off the fee before they opened the platform. They treated it like a gym membership or a course enrollment. Money spent. Value received through the attempt itself, regardless of outcome.

How Budget Pressure Breaks Your Trading

When you fear losing money you need, a predictable pattern kicks in:

You force trades. No clean setup at 10 AM? Normally you would wait. But you paid $600 you cannot afford, so you convince yourself that mediocre setup at 10:30 is "good enough." It is not.

You move your stop loss. Your plan says 30 pips. But the trade is going against you, and closing the loss means your fee is closer to gone. So you widen to 50 pips. Now a 1% risk trade is a 1.7% risk trade, and your daily loss limit is one bad trade away from breaching.

You overtrade after losses. Down $300 on the funded account after two clean losses? Your plan says stop for the day. But fee anxiety says "I need to make that back right now." You take three more trades, none of them aligned with your setup criteria.

You freeze on winners. Your trade hits 2R and your plan targets 3R. But the fear of giving back profit (and by extension, getting closer to failing) causes you to close early. Repeatedly cutting winners short destroys your expectancy over a sample of trades.

Every one of these behaviors comes from the same root: the fee was money you could not lose.

Budget for Multiple Attempts

The data is clear. Most traders fail their first funded challenge. Many fail their second and third. Planning your budget around a single attempt is planning to quit after one failure.

If your disposable income supports it, allocate enough for at least 2 to 3 attempts. Not because failure is guaranteed, but because removing the "this is my only shot" pressure improves your trading on every attempt.

Think of it like this: if you budget $300 for funded challenges over 3 months, you can attempt the $10k challenge 3 times. Each attempt costs $89 to $100. If you fail the first one, you still have two more tries without any additional financial strain.

That safety net changes your psychology. You stop treating each individual trade as a make-or-break moment and start treating the challenge as a process, which is exactly what it is.

Right-Size the Account, Not Your Ego

Ego says take the $100k account because it sounds better. Math says take the account size that lets you trade without financial pressure.

A $10,000 funded account at 1% risk per trade is $100 per trade in play. On a 3R winner, that is $300 in profit. Scale that over a month of consistent trading and you have a meaningful position sizing foundation.

You can always scale up later. Most prop firms offer scaling plans that increase your account size after consistent profitability. Starting small and scaling up is the professional approach. Starting big and blowing the fee is the amateur approach.

How EdgeFlo Helps You Trade Within Your Risk Budget

EdgeFlo's guardrails let you set daily loss limits and maximum trades per session so your funded account stays within the rules even when emotions push you to overtrade. You can override the guardrails if you choose to, but the friction makes rule-breaking a conscious decision instead of an impulsive one.

The dashboard shows your risk per trade and running daily loss in real time. When you can see exactly how much room you have before a rule violation, the urge to force trades fades because the numbers are right in front of you.

Starting a funded challenge with the right budget is step one. Protecting that budget with visible, structured risk controls is what keeps you in the game long enough to pass.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

How much should I budget for a funded challenge?

Should I start with a $100k or $10k challenge?

Why does challenge budget affect my trading?

Can I try again if I fail the challenge?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.