Think in Quarters, Not Trades: The Long-Term Trading Mindset

One trade means nothing. One quarter tells the truth. Learn how shifting your evaluation window from daily to quarterly eliminates emotional decision-making.

You just had your worst week in two months. Four losses in a row. Your account is down 3.2%, and every fiber in your body is screaming to change something. New indicator. Tighter stop. Different pair. Maybe a completely different strategy.

Sound familiar?

Here is the uncomfortable truth: you cannot evaluate a trading strategy on one week. You cannot even evaluate it on one month. The minimum window that tells you anything real about your edge is one quarter.

TL;DR

A single trade, day, or week tells you nothing about whether your strategy works.

The law of large numbers means your edge only shows up over 60 or more trades.

Quarterly evaluation (13 weeks) is the shortest window that separates signal from noise.

Changing your rules after every loss is the fastest way to guarantee you never find consistency.

Tracking monthly stats inside a quarterly frame gives you the pattern recognition you need without the emotional whiplash.

Why Your Evaluation Window Is Probably Too Short

Most traders evaluate themselves daily. Some even evaluate after every single trade. Win? The strategy works. Loss? Something must be wrong.

This is the same logic a roulette player uses. One spin lands on black, and suddenly black is "hot." One spin lands on red, and the whole plan changes.

Casinos do not think this way. A casino knows it has a 5.26% edge on every spin of the roulette wheel (20 winning outcomes out of 38 total). On any single spin, a player can win big. On any single night, the casino can lose money. But the casino does not panic after a bad Tuesday. It does not swap the roulette wheel for a different one.

Why? Because the casino evaluates over thousands of spins. It trusts the law of large numbers: given enough events, the actual results converge toward the statistical edge.

Your trading account works exactly the same way. If you have a backtested strategy with a 40% win rate and a 3:1 reward to risk, your edge is mathematically real. But that edge does not promise you four wins out of your next ten trades. It promises that over hundreds of trades, your results will cluster around 40%. The larger the sample, the tighter the cluster.

The Problem with Daily and Weekly Scorecards

When you judge yourself trade by trade, you invite every emotional bias into your decision-making. Recency bias makes your last trade feel like the most important one. Loss aversion makes a $200 loss hurt twice as much as a $200 win feels good.

Ever had a week where you followed your plan perfectly, took three textbook setups, and all three lost? That is a completely normal outcome for a 40% win rate system. The probability of three consecutive losses is 21.6%.

More than one in five stretches of three trades will be all losses. If you change your rules every time this happens, you will never stay on one system long enough to see the edge play out.

Walkthrough: The Trader Who Changed Too Fast

A GBP/USD day trader has a tested strategy: London session breakouts with a 35% win rate and 4:1 R:R. In week one, he takes four trades. Three lose, one wins.

The three losses cost 1% each (0.5% risk at 2:1 stops, but his system uses fixed 1% risk per trade). The one win returns 4%.

3 losses at 1% each = 3% drawdown

1 win at 4% = 4% gain

Net for the week: +1%

He is profitable. But it does not feel profitable because three of his four trades lost. So he tightens his entry criteria. Week two, he takes only one trade (the filter is too tight). It loses. Now he is down 1% on the week, and he panics.

By week three, he has abandoned the strategy entirely. He never reached the 50 to 60 trade sample that would have shown his edge.

This trader did not have a strategy problem. He had an evaluation window problem.

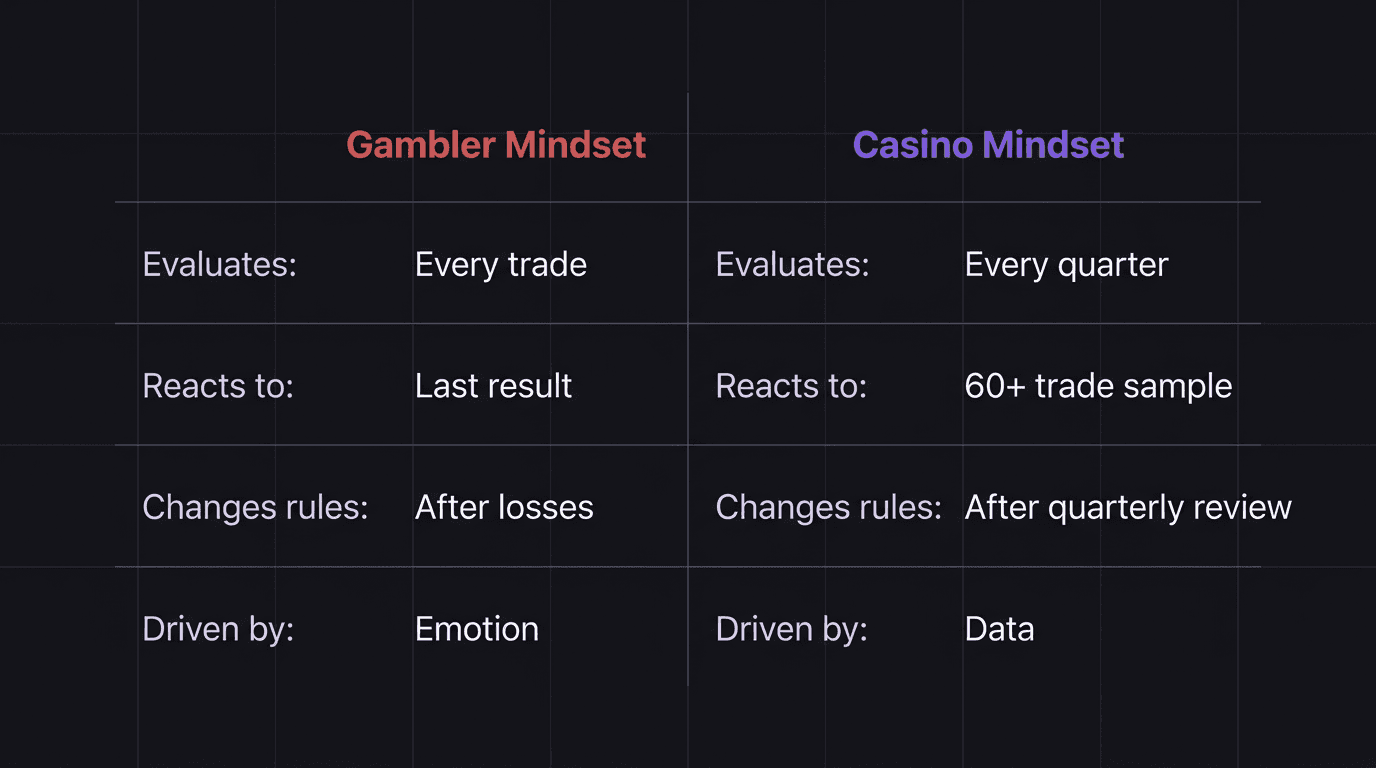

Think Like the House, Not the Player

The difference between a casino and a gambler is not luck. It is time horizon.

A gambler evaluates hand by hand. Win big, push harder. Lose big, chase the money back. The gambler's emotional state drives every decision.

A casino evaluates quarter by quarter. It tracks revenue, expenses, and net profit over 90-day windows. A bad weekend does not trigger a rules change. A bad month gets noted and reviewed at the quarterly mark.

You need to adopt the casino's approach. Set your rules, execute them consistently for a full quarter, and only then evaluate whether the strategy is working. That means 13 weeks. Roughly 60 trading days. If you take one or two trades per day, that gives you 60 to 120 trades, which is enough for the law of large numbers to start smoothing out variance.

How to Build a Quarterly Evaluation System

Shifting from daily judgment to quarterly evaluation does not mean you ignore your results for three months. It means you collect data weekly, review monthly, and make decisions quarterly.

Step 1: Track Weekly, Do Not Judge Weekly

Every Friday, record the basics: number of trades, win rate, average R gained, average R lost, and whether you followed your plan on each trade. This is data collection, not a performance review. You are building the dataset your quarterly review will use.

Think of yourself as a scientist running an experiment. You would not declare the hypothesis wrong after two data points. You would collect 60 data points and then analyze.

Step 2: Review Monthly for Patterns

Once a month, look at the weekly numbers together. Are there any patterns? Did week three have a spike in off-plan trades? Did your win rate drop during high-impact news weeks?

Monthly reviews are for pattern recognition, not strategy changes. You are looking for process leaks, not outcome problems. Set clear trading goals at the monthly level that focus on execution quality rather than P&L.

Step 3: Decide Quarterly

At the end of 13 weeks, pull the full dataset. Now you have enough trades to answer the real questions:

Is my actual win rate within 5% of my backtested win rate?

Is my average R:R holding steady?

Am I following my plan on 80% or more of my trades?

Where are the process breakdowns concentrated?

If the numbers hold up, keep going. If the numbers show consistent drift across the full quarter, now you have earned the right to adjust.

Walkthrough: What a Quarterly Review Looks Like

A EUR/USD swing trader risks 1% per trade with a target of 3:1. Over 13 weeks, she takes 48 trades.

Wins: 20 out of 48 = 41.7% win rate

Average win: 2.8R

Average loss: 1.0R

Plan adherence: 42 out of 48 trades followed the plan (87.5%)

6 off-plan trades: 1 win, 5 losses

Her expectancy is 0.58R per trade. Over 48 trades, that is roughly 28R in net profit. At 1% risk, that is a 28% account gain over the quarter.

But buried inside that profitable quarter were two losing weeks in a row during weeks 5 and 6. If she had evaluated weekly, she might have panicked and changed strategies right before the profitable run in weeks 7 through 10.

The quarterly view told the real story. The weekly view would have lied.

The Math That Proves Short-Term Results Are Noise

Here is why a 40% win rate feels so unreliable on small samples. If you flip a biased coin that lands heads 40% of the time, the possible outcomes over 5 flips look wild:

0 heads out of 5: 7.8% probability

1 head out of 5: 25.9% probability

2 heads out of 5: 34.6% probability

3 heads out of 5: 23.0% probability

Over just 5 trades, there is a 33.7% chance you get 0 or 1 wins. One-third of the time, your perfectly good 40% strategy looks like a 0 to 20% strategy. That is noise pretending to be signal.

Now run 100 trades. The probability of your observed win rate being between 35% and 45% jumps dramatically. The noise shrinks. The signal emerges.

This is why thinking in probabilities is not just a nice idea. It is the mathematical foundation of every profitable trading career.

What Quarterly Thinking Does to Your Emotions

When you stretch your evaluation window from days to quarters, something unexpected happens: you stop caring about individual trades.

Not in a reckless way. You still execute with precision. You still manage risk. But the emotional weight of each trade drops because you know one trade is one data point in a 60-trade sample. It carries roughly 1.7% of the information you need.

Losses stop triggering rule changes. Wins stop triggering overconfidence. You develop what experienced traders call "outcome independence," and it is not a personality trait. It is a direct consequence of choosing the right evaluation window.

Trading consistency is not about being right more often. It is about executing the same process long enough for the math to work.

The Quarterly Review Checklist

Use this at the end of every 13-week cycle:

Total trades taken vs. expected trade frequency

Actual win rate vs. backtested win rate (is it within 5%?)

Average R:R on wins vs. planned R:R

Plan adherence rate (target: 85% or higher)

Off-plan trade outcomes (almost always worse than on-plan)

Worst drawdown during the quarter and what triggered it

Best streak during the quarter and whether you over-leveraged during it

If four or more of these metrics are on track, your system is working. Refine the edges. Do not rebuild.

If three or more are off track across the full quarter, you have a real signal that something needs to change. Now you can adjust with data instead of emotion.

How EdgeFlo Supports Quarterly Thinking

EdgeFlo's Dashboard shows your performance over time, not just today's P&L. Win rate, average R, profit factor, and discipline metrics accumulate across weeks and months, giving you the quarterly view without building spreadsheets from scratch.

The Journal's weekly AI report (Plus) surfaces trends across multiple sessions. Instead of reacting to your last trade, you see patterns forming over 5, 10, or 20 sessions. That is the kind of feedback that makes quarterly reviews productive instead of guesswork.

When your evaluation window matches your edge's sample size requirement, every review session becomes a genuine decision point instead of an emotional reaction.

The Edge Brief

Receive Insights on trading psychology, discipline, and the behavioral patterns that create consistent traders from our Founder and the EdgeFlo team, delivered to your inbox.

Think different. Trade different.

How long should I evaluate my trading performance?

Why does one bad week feel so devastating?

Should I change my strategy after a losing month?

What is the law of large numbers in trading?

Turn discipline on.

Every session.

EdgeFlo is the environment serious traders operate inside.

Start 7-Day Trial — $7

Cancel anytime.

No long-term commitment.

Think Different, Trade Different.